Global Steel Alloys Market - Size and Forecast Analysis, 2021-2035

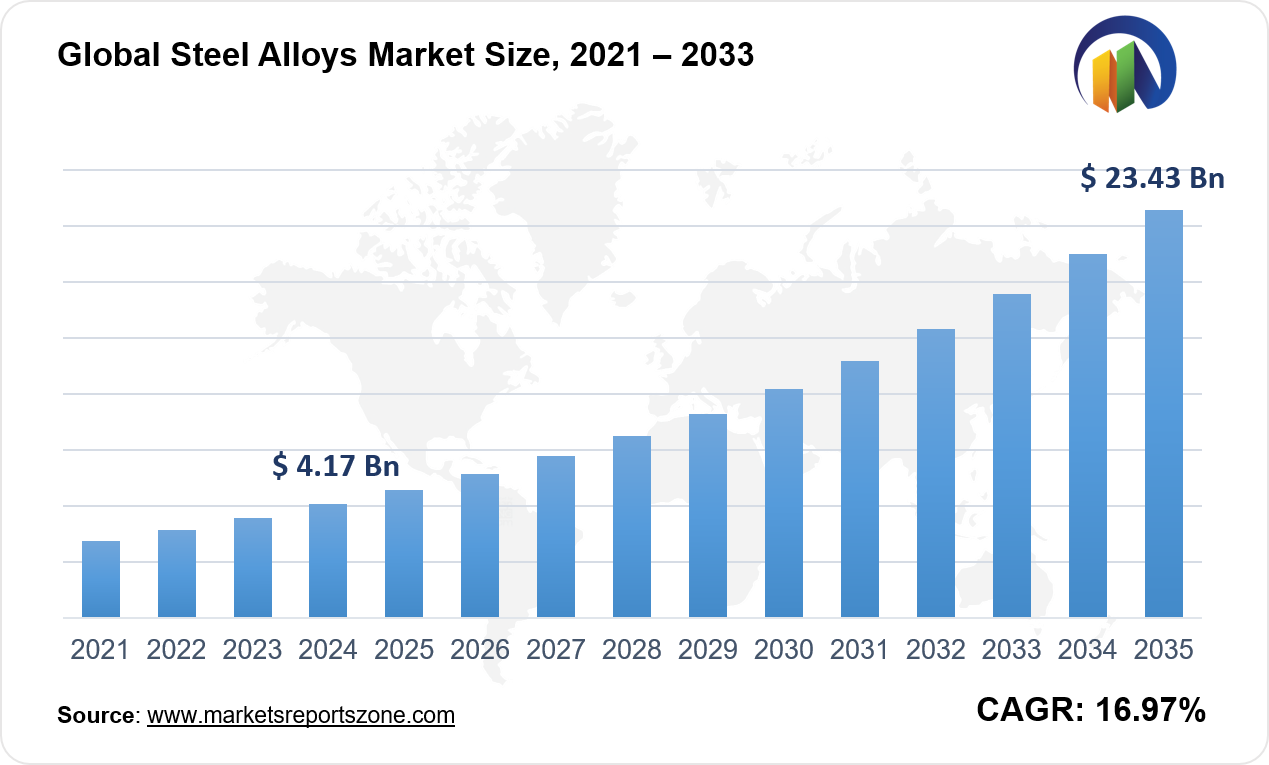

Global Steel Alloys Market Size is expected to reach USD 23.43 Billion by 2035 from USD 4.17 Billion in 2024, with a CAGR of around 16.97% between 2024 and 2035. The global steel alloys market is driven by rising demand in construction and increasing automotive production. High-strength steel alloys are widely used in skyscrapers and bridges to enhance durability. In the automotive sector, lightweight steel alloys are being adopted to improve fuel efficiency and vehicle performance. However, fluctuating raw material prices act as a major restraint, affecting production costs and profitability. Opportunities exist with advancements in recycling technology, where scrap steel is being efficiently repurposed to reduce environmental impact. The growing renewable energy sector also boosts demand, as steel alloys are essential in wind turbines and solar panel structures. In aerospace, titanium-steel alloys are enhancing aircraft strength while reducing weight. Rail infrastructure projects in developing nations are increasing the need for corrosion-resistant steel alloys. Manufacturers are investing in advanced metallurgical processes to enhance alloy properties, catering to diverse industrial needs. The shipbuilding industry relies on high-strength, weather-resistant steel alloys for improved vessel longevity. Governments worldwide are supporting steel production through favorable policies and infrastructure investments. The market continues to evolve as industries seek stronger, more sustainable materials for critical applications. Innovations in alloy composition are further expanding the potential of steel alloys across multiple sectors.

Driver: Rising Construction Demand Fuels Growth

The increasing demand for steel alloys in construction is a key driver of market growth. Modern infrastructure projects require high-strength, corrosion-resistant materials to ensure longevity and safety. Steel alloys are widely used in high-rise buildings, tunnels, and bridges due to their superior mechanical properties. In earthquake-prone regions, seismic-resistant steel alloys are being incorporated into structures to enhance durability against tremors. Skyscrapers like those in Dubai and New York utilize advanced steel alloys to support extreme heights while maintaining structural integrity. The demand for sustainable construction materials is also rising, leading to the use of recycled steel alloys in green building projects. In railway expansion projects, wear-resistant steel alloys are being used for tracks to increase lifespan and reduce maintenance costs. Bridges such as the Millau Viaduct in France and the Akashi Kaikyō Bridge in Japan rely on specialized steel alloys to withstand heavy loads and harsh weather conditions. Prefabricated steel structures are becoming more popular, reducing construction time and costs. Governments worldwide are investing in smart cities and urban infrastructure, further driving the demand for steel alloys. As construction activities continue to rise, innovations in steel alloy composition are enhancing both performance and sustainability.

Key Insights:

- The adoption rate of steel alloys across various industries is estimated to be around 35% as of 2024.

- Government investments in the development of advanced steel alloy technologies have reached approximately $400 million in recent years.

- In 2023, the total number of steel alloy units sold was around 200 million tons globally.

- The penetration rate of steel alloys in the automotive industry is about 50%, reflecting their critical role in vehicle manufacturing.

- Approximately 80% of construction projects are utilizing steel alloys for structural applications, highlighting their importance in infrastructure development.

- The annual growth rate for investments in research and development for innovative steel alloys is projected to be around 7% over the next five years.

- Surveys indicate that nearly 60% of manufacturers are actively integrating high-performance steel alloys into their production processes.

- The aerospace sector is increasingly adopting steel alloys, with an expected increase in usage by 15% annually through 2026.

Segment Analysis:

Steel alloys play a vital role across various industries, with different compositions catering to specific needs. Binary alloys, made from two primary elements, are widely used in pipelines and structural components due to their balance of strength and flexibility. Ternary alloys, incorporating three elements, are preferred in the automotive and aerospace sectors for their enhanced durability and heat resistance. Multielement alloys, containing multiple metals, are in high demand for extreme environments, such as deep-sea drilling and space exploration, where corrosion and pressure resistance are crucial. The aviation industry extensively uses lightweight, high-strength steel alloys in aircraft fuselages and landing gears to improve fuel efficiency and safety. The military industry relies on hardened steel alloys for armored vehicles, naval ships, and missile systems, ensuring superior protection and longevity in combat environments. In industrial manufacturing, wear-resistant alloys are essential in heavy machinery, reducing downtime and maintenance costs in mining and construction equipment. The medical industry benefits from biocompatible steel alloys used in surgical instruments, orthopedic implants, and dental braces, ensuring durability and patient safety. As industries continue to evolve, innovations in alloy composition and processing techniques are enhancing the performance, efficiency, and sustainability of steel alloys worldwide.

Regional Analysis:

The global steel alloys market is expanding across all regions, driven by industrial growth and infrastructure projects. In North America, aerospace and defense sectors heavily invest in advanced steel alloys for aircraft components and military equipment. The United States uses high-strength alloys in space missions, with NASA incorporating them into rocket structures for durability. Europe sees strong demand from the automotive industry, with Germany and France using lightweight steel alloys to produce fuel-efficient cars and electric vehicle frames. The Asia-Pacific region leads in steel production, with China and India using multielement alloys in large-scale railway and high-speed train projects. Japan’s shipbuilding industry also relies on corrosion-resistant alloys to enhance vessel longevity. In Latin America, growing industrialization fuels demand for wear-resistant steel alloys in mining and oil drilling operations, especially in Brazil and Chile. The Middle East and Africa are witnessing increased use of heat-resistant steel alloys in power plants and petrochemical industries. The UAE utilizes advanced alloys in skyscrapers like the Burj Khalifa, ensuring stability against extreme temperatures. As global industries continue evolving, the demand for stronger, more efficient steel alloys is driving innovation in material engineering and advanced manufacturing processes.

Competitive Scenario:

The global steel alloys market is experiencing significant advancements, driven by key industry players. Nippon Steel is actively pursuing a $15 billion bid to acquire U.S. Steel, aiming to expand its presence in overseas markets such as India, Southeast Asia, and the U.S. ArcelorMittal, in collaboration with Nippon Steel, acquired Essar Steel, enhancing its footprint in the Indian market.Nucor Corporation focuses on sustainable practices, investing in electric arc furnace technology to produce steel alloys with reduced carbon emissions. Baosteel Group has developed advanced high-strength steels, catering to the automotive industry's demand for lightweight yet durable materials. Thyssenkrupp Aerospace supplies tailored steel alloy products to the aerospace sector, ensuring materials meet stringent safety and performance standards. Kobe Steel has introduced innovative steel alloys for the construction industry, enhancing structural integrity and resilience. Materion specializes in high-performance alloys for the medical sector, providing materials for implants and surgical instruments. Aperam focuses on producing stainless steel alloys with improved corrosion resistance, serving the chemical and food processing industries. Carpenter Technology Corporation develops specialty steel alloys for the energy sector, including materials for oil and gas exploration. These companies' strategic initiatives and innovations are collectively driving the evolution and growth of the steel alloys market across various applications.

Steel Alloys Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 4.17 Billion |

| Revenue Forecast in 2035 | USD 23.43 Billion |

| Growth Rate | CAGR of 16.97% from 2025 to 2035 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2035 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | AMI Metals; Arcelor Mittal; Nippon Steel & Sumitomo Metal; Nucor Corporation; Baosteel Group; Thyssenkrupp Aerospace; Kobe Steel; Materion; Aperam; Carpenter |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Steel Alloys Market report is segmented as follows:

By Type,

- Binary Alloy

- Ternary Alloy

- Multielement Alloy

By Application,

- Aviation Industry

- Military Industry

- Industrial Manufacture

- Medical Industry

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East and Africa

Key Market Players,

- AMI Metals

- Arcelor Mittal

- Nippon Steel & Sumitomo Metal

- Nucor Corporation

- Baosteel Group

- Thyssenkrupp Aerospace

- Kobe Steel

- Materion

- Aperam

- Carpenter

Frequently Asked Questions

How big is the Steel Alloys market?

Global Steel Alloys Market Size was valued at USD 4.17 Billion in 2024 and is projected to reach at USD 23.43 Billion in 2035.

What is the Steel Alloys market growth?

Global Steel Alloys Market is expected to grow at a CAGR of around 16.97% during the forecasted year.

Which region has the largest market share in Steel Alloys market?

North America, Asia Pacific and Europe are major regions in the global Steel Alloys Market.

Who are the key players in Steel Alloys market?

Key players analyzed in the global Steel Alloys Market are AMI Metals; Arcelor Mittal; Nippon Steel & Sumitomo Metal; Nucor Corporation; Baosteel Group; Thyssenkrupp Aerospace; Kobe Steel; Materion; Aperam; Carpenter and so on.