Global Semiconductor Market, By Device Type (Integrated Circuits (ICs), Discrete Semiconductors, Optoelectronics, Sensors, Others), By Application, and By Region - Trends and Forecast Analysis, 2021-2033

Publish Date: 2025-03-02 | Format: PDF | Category: Electronic and Semiconductor | Pages: 324

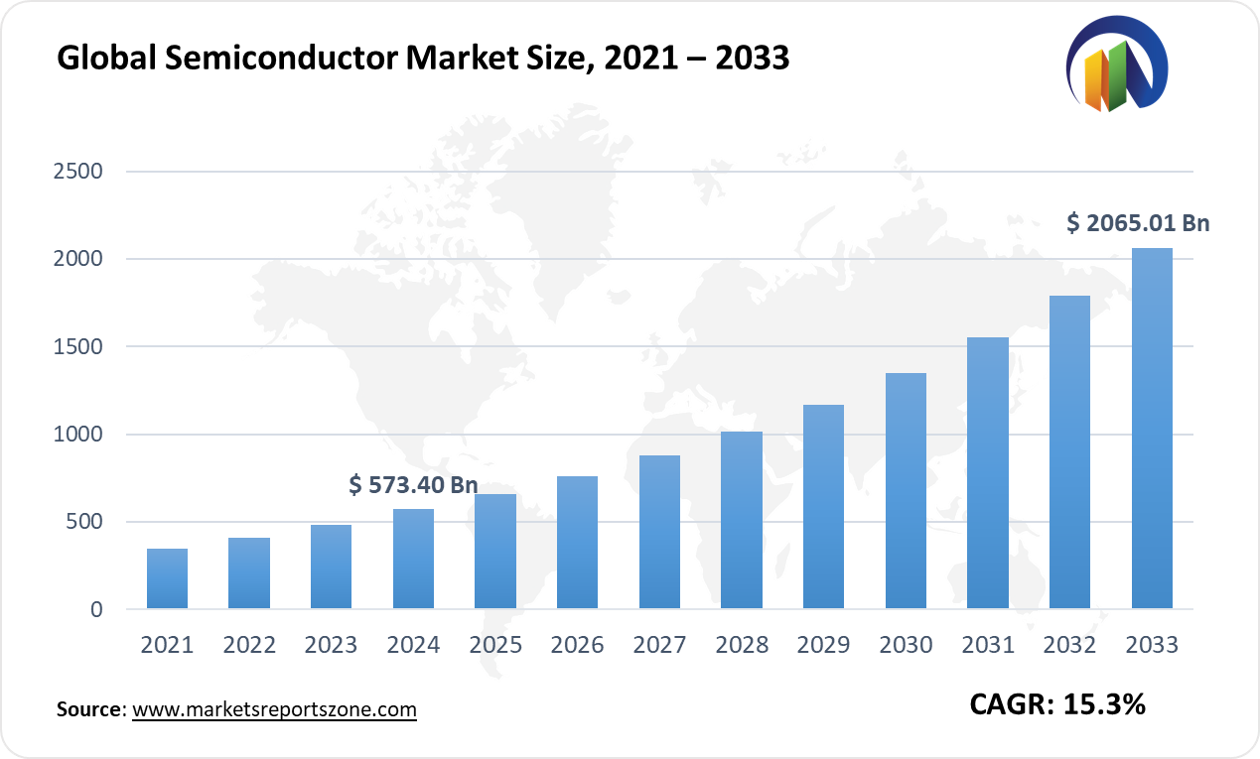

The Global Semiconductor Market was valued at USD 573.4 Billion in 2024 and is projected to reach USD 2065.0 Billion by 2033 at a CAGR of around 15.3% between 2024 and 2033. The global semiconductor market is driven by the rising demand for consumer electronics and advancements in artificial intelligence. Smartphones, laptops, and gaming consoles rely on high-performance chips, increasing semiconductor production. AI-powered applications in healthcare, automation, and robotics further boost adoption. However, supply chain disruptions act as a major restraint. Shortages in raw materials, chip fabrication delays, and geopolitical tensions limit manufacturing capacity, causing delays in product launches. Opportunities arise with the expansion of 5G technology and the growing adoption of electric vehicles. 5G networks require advanced semiconductors for high-speed data processing, enhancing connectivity worldwide.

EV manufacturers integrate high-efficiency chips in battery management and autonomous driving systems, improving vehicle performance. In real-life applications, semiconductor-based processors enable smart home devices, enhancing automation and user convenience. Cloud computing infrastructure depends on high-end chips to manage massive data loads efficiently. Modern cars use semiconductor sensors in collision detection and self-parking technologies, ensuring road safety. Aerospace and defense industries incorporate semiconductors in navigation, missile guidance, and satellite communication systems. Wearable technology, including smart glasses and biometric devices, relies on semiconductor advancements for improved functionality. As digital transformation accelerates, continuous research and innovation in semiconductor technology drive further market growth.

Driver: AI Revolution Fuels Semiconductor Growth

Artificial intelligence (AI) is transforming industries, driving massive demand for advanced semiconductors. AI-powered applications require high-performance chips to process large amounts of data efficiently. Machine learning models depend on powerful GPUs and AI-specific processors to execute complex computations. Data centers invest in high-speed semiconductor chips to support AI-driven cloud computing and big data analytics. Autonomous robots in warehouses use AI chips for real-time decision-making, improving efficiency in logistics. Smart cities rely on AI-enabled semiconductors for traffic management and surveillance systems, enhancing public safety. In financial services, AI-powered trading algorithms process market data rapidly, requiring advanced chipsets for real-time execution.

AI-assisted medical imaging in hospitals uses semiconductor-based processors to detect diseases with higher accuracy. Personal assistants like AI chatbots and voice recognition systems function seamlessly with semiconductor advancements. AI-driven cybersecurity systems analyze threats instantly, providing enhanced protection for businesses. Drones equipped with AI chips perform automated inspections in agriculture and infrastructure. AI-powered translation devices enable real-time communication across languages, improving global connectivity. As AI adoption expands, the semiconductor industry continues to evolve. Companies invest in research to develop faster and more energy-efficient AI processors. The future of AI-driven innovations depends on cutting-edge semiconductor technology.

Key Insights:

- In 2021, global semiconductor unit sales reached a historic 1.15 trillion units, reflecting robust demand across various sectors.

- The semiconductor industry consistently invests between 15-20% of its sales revenue into research and development, underscoring its commitment to innovation.

- In 2022, TSMC increased its R&D investment to US $5.47 billion to extend its technology leadership and differentiation.

- In 2023, sales by U.S.-headquartered semiconductor firms grew to $264.6 billion, marking a compound annual growth rate of 6.0% since 2001.

- In August 2023, TSMC announced plans to invest in the European Semiconductor Manufacturing Company (ESMC) GmbH in Dresden, Germany, alongside Robert Bosch GmbH, Infineon Technologies AG, and NXP Semiconductors N.V., with total investments expected to exceed 10 billion Euros.

- From 2025 to 2027, semiconductor manufacturers are projected to spend a record $400 billion on chip-making equipment, with China, South Korea, and Taiwan leading the investments.

- In May 2020, TSMC announced plans to invest $12 billion in Phoenix, Arizona, to build an advanced semiconductor manufacturing fabrication, later increasing the total investment to $40 billion with the addition of a second fab.

- In Q2 2024, integrated circuit (IC) sales showed robust 27% year-over-year growth and are expected to surge 29% in Q3 2024, surpassing record levels seen in 2021

Segment Analysis:

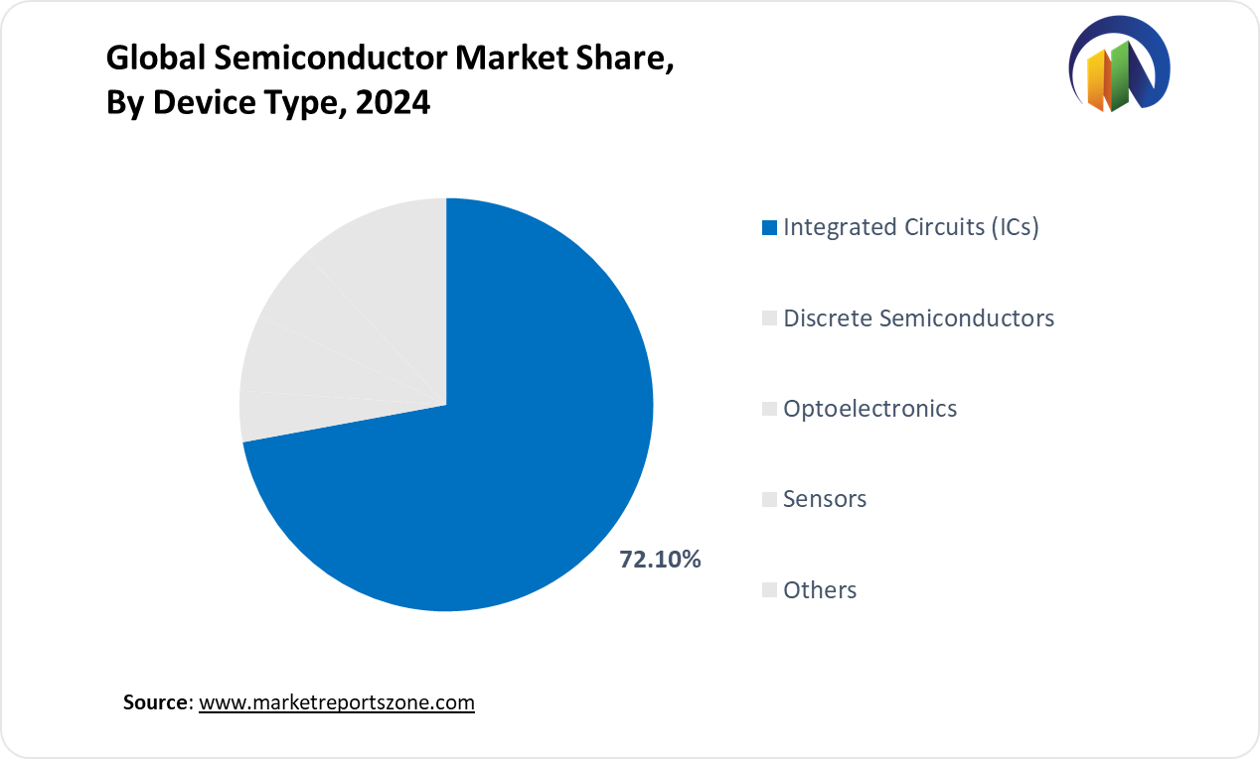

The semiconductor market is diverse, with various device types and applications shaping its growth. Integrated Circuits (ICs) dominate, powering everything from high-speed computing to smart appliances. In data centers, AI processors optimize cloud storage and real-time analytics. Discrete semiconductors play a crucial role in power management, ensuring stable energy flow in industrial automation. Factories use these components in robotic arms for seamless operations. Optoelectronics enable high-speed communication, making fiber-optic networks essential for telecom infrastructure. In smart cities, optoelectronic sensors manage intelligent street lighting for energy efficiency.

Sensors drive advancements in automotive safety, with LiDAR sensors used in autonomous vehicles for precise navigation. Industrial IoT systems rely on sensors for predictive maintenance, preventing costly downtime. Consumer electronics thrive on semiconductor advancements, with smart TVs integrating AI chips for enhanced user experience. Telecom & infrastructure demand high-frequency chips for seamless 5G connectivity, ensuring low-latency communication. Automotive innovations depend on semiconductors for electric vehicle battery efficiency and advanced driver assistance systems. Industrial applications use rugged semiconductors to withstand extreme temperatures in manufacturing plants. As technology advances, demand for high-performance semiconductor devices continues to rise, driving innovation across industries and reshaping the future of digital transformation.

Regional Analysis:

The semiconductor market varies across regions, driven by technology adoption and industrial advancements. North America leads in innovation, with major companies investing in AI-powered chips. Self-driving car tests in California rely on advanced semiconductors for real-time data processing. Europe focuses on sustainability, integrating power-efficient chips in smart grids and renewable energy projects. Wind farms in Germany use semiconductor-based converters for efficient electricity transmission. Asia-Pacific dominates manufacturing, with countries like Taiwan and South Korea producing cutting-edge semiconductors. In Japan, industrial robots use high-speed chips for precision automation in automotive factories.

Latin America sees growing semiconductor use in telecom and consumer electronics. Brazil’s expanding 5G networks depend on semiconductor-powered base stations for uninterrupted connectivity. The Middle East & Africa prioritize semiconductor adoption in defense and infrastructure. The UAE’s space programs use semiconductor-based satellite communication systems for deep-space exploration. Across all regions, demand for semiconductors continues to rise, driven by AI, IoT, and automotive advancements. Governments invest in domestic production to strengthen supply chains and reduce dependency on imports. As digital transformation accelerates, the semiconductor industry remains at the core of technological progress, shaping the future of global innovation and connectivity.

Competitive Scenario:

Leading semiconductor companies are driving innovation through advanced chip designs, AI integration, and expanded production capacity. Broadcom focuses on high-performance networking chips, enhancing data center efficiency. Samsung Electronics advances memory technology, with next-gen DRAM improving smartphone and AI computing speeds. Intel Corporation invests in new fabrication plants, strengthening domestic chip production. Maxim Integrated develops power-efficient ICs, optimizing industrial automation and automotive applications. Taiwan Semiconductors (TSMC) expands its foundry operations, producing cutting-edge 3nm and 2nm chips for global tech giants. Micron Technology enhances NAND and DRAM solutions, boosting storage performance in cloud computing.

NXP Semiconductors innovates in automotive chips, enabling enhanced safety features in self-driving vehicles. NVIDIA leads in AI-driven GPUs, powering deep learning models and autonomous systems. Qualcomm advances 5G modem technology, ensuring faster connectivity in mobile and IoT devices. SK Hynix refines high-bandwidth memory solutions, improving performance for AI and graphics applications. Texas Instruments focuses on embedded processors for industrial automation and medical devices. Toshiba strengthens power semiconductor production, supporting renewable energy systems. Companies continue to invest in R&D, ensuring semiconductor advancements across consumer electronics, automotive, AI, and cloud computing. With continuous technological evolution, semiconductor firms shape the future of digital transformation.

Semiconductor Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 573.4 Billion |

| Revenue Forecast in 2033 | USD 2065.0 Billion |

| Growth Rate | CAGR of 15.3% from 2025 to 2033 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2033 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | Broadcom, Inc.; Samsung Electronics; Intel Corporation; Maxim Integrated Products, Inc.; Taiwan Semiconductors; Micron Technology; NXP Semiconductors N.V.; NVIDIA Corporation; Qualcomm; SK Hynix; Texas Instruments; Toshiba Corporation; Others |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Semiconductor Market report is segmented as follows:

By Device Type,

- Integrated Circuits (ICs)

- Discrete Semiconductors

- Optoelectronics

- Sensors

- Others

By Application,

- Data Centers

- Consumer Electronics

- Telecom & Infrastructure

- Automotive

- Industrial

- Others

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East & Africa

Key Market Players,

- Broadcom, Inc.

- Samsung Electronics

- Intel Corporation

- Maxim Integrated Products, Inc.

- Taiwan Semiconductors

- Micron Technology

- NXP Semiconductors N.V.

- NVIDIA Corporation

- Qualcomm

- SK Hynix

- Texas Instruments

- Toshiba Corporation

- Others

Frequently Asked Questions

Research Objectives

- Proliferation and maturation of trade in the global Semiconductor Market.

- The market share of the global Semiconductor Market, supply and demand ratio, growth revenue, supply chain analysis, and business overview.

- Current and future market trends that are influencing the growth opportunities and growth rate of the global Semiconductor Market.

- Feasibility study, new market insights, company profiles, investment return, market size of the global Semiconductor Market.

Chapter 1 Semiconductor Market Executive Summary

- 1.1 Semiconductor Market Research Scope

- 1.2 Semiconductor Market Estimates and Forecast (2021-2033)

- 1.2.1 Global Semiconductor Market Value and Volume and Growth Rate (2021-2033)

- 1.2.2 Global Semiconductor Market Price Trend (2021-2033)

- 1.3 Global Semiconductor Market Value and Volume Comparison, by Device Type (2021-2033)

- 1.3.1 Integrated Circuits (ICs)

- 1.3.2 Discrete Semiconductors

- 1.3.3 Optoelectronics

- 1.3.4 Sensors

- 1.3.5 Others

- 1.4 Global Semiconductor Market Value and Volume Comparison, by Application (2021-2033)

- 1.4.1 Data Centers

- 1.4.2 Consumer Electronics

- 1.4.3 Telecom & Infrastructure

- 1.4.4 Automotive

- 1.4.5 Industrial

- 1.4.6 Others

Chapter 2 Research Methodology

- 2.1 Introduction

- 2.2 Data Capture Sources

- 2.2.1 Primary Sources

- 2.2.2 Secondary Sources

- 2.3 Market Size Estimation

- 2.4 Market Forecast

- 2.5 Assumptions and Limitations

Chapter 3 Market Dynamics

- 3.1 Market Trends

- 3.2 Opportunities and Drivers

- 3.3 Challenges

- 3.4 Market Restraints

- 3.5 Porter's Five Forces Analysis

Chapter 4 Supply Chain Analysis and Marketing Channels

- 4.1 Semiconductor Supply Chain Analysis

- 4.2 Marketing Channels

- 4.3 Semiconductor Suppliers List

- 4.4 Semiconductor Distributors List

- 4.5 Semiconductor Customers

Chapter 5 COVID-19 & Russia–Ukraine War Impact Analysis

- 5.1 COVID-19 Impact Analysis on Semiconductor Market

- 5.2 Russia-Ukraine War Impact Analysis on Semiconductor Market

Chapter 6 Semiconductor Market Estimate and Forecast by Region

- 6.1 Global Semiconductor Market Value by Region: 2021 VS 2023 VS 2033

- 6.2 Global Semiconductor Market Scenario by Region (2021-2023)

- 6.2.1 Global Semiconductor Market Value and Volume Share by Region (2021-2023)

- 6.3 Global Semiconductor Market Forecast by Region (2024-2033)

- 6.3.1 Global Semiconductor Market Value and Volume Forecast by Region (2024-2033)

- 6.4 Geographic Market Analysis: Market Facts and Figures

- 6.4.1 North America Semiconductor Market Estimates and Projections (2021-2033)

- 6.4.2 Europe Semiconductor Market Estimates and Projections (2021-2033)

- 6.4.3 Asia Pacific Semiconductor Market Estimates and Projections (2021-2033)

- 6.4.4 Latin America Semiconductor Market Estimates and Projections (2021-2033)

- 6.4.5 Middle East & Africa Semiconductor Market Estimates and Projections (2021-2033)

Chapter 7 Global Semiconductor Competition Landscape by Players

- 7.1 Global Top Semiconductor Players by Value (2021-2023)

- 7.2 Semiconductor Headquarters and Sales Region by Company

- 7.3 Company Recent Developments, Mergers & Acquisitions, and Expansion Plans

Chapter 8 Global Semiconductor Market, by Device Type

- 8.1 Global Semiconductor Market Value and Volume, by Device Type (2021-2033)

- 8.1.1 Integrated Circuits (ICs)

- 8.1.2 Discrete Semiconductors

- 8.1.3 Optoelectronics

- 8.1.4 Sensors

- 8.1.5 Others

Chapter 9 Global Semiconductor Market, by Application

- 9.1 Global Semiconductor Market Value and Volume, by Application (2021-2033)

- 9.1.1 Data Centers

- 9.1.2 Consumer Electronics

- 9.1.3 Telecom & Infrastructure

- 9.1.4 Automotive

- 9.1.5 Industrial

- 9.1.6 Others

Chapter 10 North America Semiconductor Market

- 10.1 Overview

- 10.2 North America Semiconductor Market Value and Volume, by Country (2021-2033)

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 North America Semiconductor Market Value and Volume, by Device Type (2021-2033)

- 10.3.1 Integrated Circuits (ICs)

- 10.3.2 Discrete Semiconductors

- 10.3.3 Optoelectronics

- 10.3.4 Sensors

- 10.3.5 Others

- 10.4 North America Semiconductor Market Value and Volume, by Application (2021-2033)

- 10.4.1 Data Centers

- 10.4.2 Consumer Electronics

- 10.4.3 Telecom & Infrastructure

- 10.4.4 Automotive

- 10.4.5 Industrial

- 10.4.6 Others

Chapter 11 Europe Semiconductor Market

- 11.1 Overview

- 11.2 Europe Semiconductor Market Value and Volume, by Country (2021-2033)

- 11.2.1 UK

- 11.2.2 Germany

- 11.2.3 France

- 11.2.4 Spain

- 11.2.5 Italy

- 11.2.6 Russia

- 11.2.7 Rest of Europe

- 11.3 Europe Semiconductor Market Value and Volume, by Device Type (2021-2033)

- 11.3.1 Integrated Circuits (ICs)

- 11.3.2 Discrete Semiconductors

- 11.3.3 Optoelectronics

- 11.3.4 Sensors

- 11.3.5 Others

- 11.4 Europe Semiconductor Market Value and Volume, by Application (2021-2033)

- 11.4.1 Data Centers

- 11.4.2 Consumer Electronics

- 11.4.3 Telecom & Infrastructure

- 11.4.4 Automotive

- 11.4.5 Industrial

- 11.4.6 Others

Chapter 12 Asia Pacific Semiconductor Market

- 12.1 Overview

- 12.2 Asia Pacific Semiconductor Market Value and Volume, by Country (2021-2033)

- 12.2.1 China

- 12.2.2 Japan

- 12.2.3 India

- 12.2.4 South Korea

- 12.2.5 Australia

- 12.2.6 Southeast Asia

- 12.2.7 Rest of Asia Pacific

- 12.3 Asia Pacific Semiconductor Market Value and Volume, by Device Type (2021-2033)

- 12.3.1 Integrated Circuits (ICs)

- 12.3.2 Discrete Semiconductors

- 12.3.3 Optoelectronics

- 12.3.4 Sensors

- 12.3.5 Others

- 12.4 Asia Pacific Semiconductor Market Value and Volume, by Application (2021-2033)

- 12.4.1 Data Centers

- 12.4.2 Consumer Electronics

- 12.4.3 Telecom & Infrastructure

- 12.4.4 Automotive

- 12.4.5 Industrial

- 12.4.6 Others

Chapter 13 Latin America Semiconductor Market

- 13.1 Overview

- 13.2 Latin America Semiconductor Market Value and Volume, by Country (2021-2033)

- 13.2.1 Brazil

- 13.2.2 Argentina

- 13.2.3 Rest of Latin America

- 13.3 Latin America Semiconductor Market Value and Volume, by Device Type (2021-2033)

- 13.3.1 Integrated Circuits (ICs)

- 13.3.2 Discrete Semiconductors

- 13.3.3 Optoelectronics

- 13.3.4 Sensors

- 13.3.5 Others

- 13.4 Latin America Semiconductor Market Value and Volume, by Application (2021-2033)

- 13.4.1 Data Centers

- 13.4.2 Consumer Electronics

- 13.4.3 Telecom & Infrastructure

- 13.4.4 Automotive

- 13.4.5 Industrial

- 13.4.6 Others

Chapter 14 Middle East & Africa Semiconductor Market

- 14.1 Overview

- 14.2 Middle East & Africa Semiconductor Market Value and Volume, by Country (2021-2033)

- 14.2.1 Saudi Arabia

- 14.2.2 UAE

- 14.2.3 South Africa

- 14.2.4 Rest of Middle East & Africa

- 14.3 Middle East & Africa Semiconductor Market Value and Volume, by Device Type (2021-2033)

- 14.3.1 Integrated Circuits (ICs)

- 14.3.2 Discrete Semiconductors

- 14.3.3 Optoelectronics

- 14.3.4 Sensors

- 14.3.5 Others

- 14.4 Middle East & Africa Semiconductor Market Value and Volume, by Application (2021-2033)

- 14.4.1 Data Centers

- 14.4.2 Consumer Electronics

- 14.4.3 Telecom & Infrastructure

- 14.4.4 Automotive

- 14.4.5 Industrial

- 14.4.6 Others

Chapter 15 Company Profiles and Market Share Analysis: (Business Overview, Market Share Analysis, Products/Services Offered, Recent Developments)

- 15.1 Broadcom, Inc.

- 15.2 Samsung Electronics

- 15.3 Intel Corporation

- 15.4 Maxim Integrated Products, Inc.

- 15.5 Taiwan Semiconductors

- 15.6 Micron Technology

- 15.7 NXP Semiconductors N.V.

- 15.8 NVIDIA Corporation

- 15.9 Qualcomm

- 15.10 SK Hynix

- 15.11 Texas Instruments

- 15.12 Toshiba Corporation

- 15.13 Others

Report ID:

18

Published Date:

March 2025

Trusted by more than 10,500 organizations globally

Infaluble Methodology

Customization

Analyst Support

Targeted Market View