Global Radiation Hardened Electronics and Semiconductors Market, By Type (Processors & Controllers, Logic, Memory, Power Management, ASICs), By Application, and By Region - Trends and Forecast Analysis, 2021-2035

Publish Date: 2025-03-28 | Format: PDF | Category: Machinery and Equipment | Pages: 377

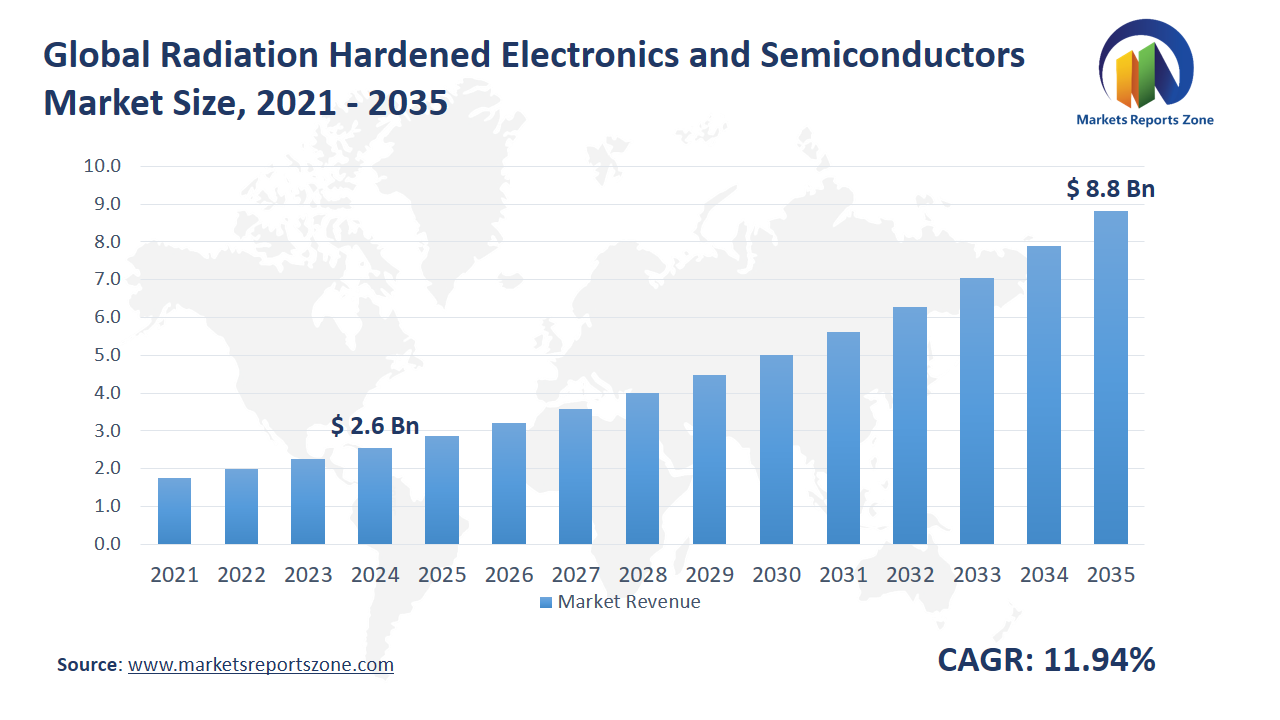

Global Radiation Hardened Electronics and Semiconductors Market Size is expected to reach USD 8.84 Billion by 2035 from USD 2.55 Billion in 2024, with a CAGR of around 11.94% between 2024 and 2035. The global radiation-hardened electronics and semiconductors market is driven by the growing demand for space exploration and the rising adoption of defense applications. Increased satellite launches and deep-space missions are fueling the need for radiation-resistant components to withstand harsh cosmic environments. In defense, military-grade electronics are being equipped with radiation-hardened semiconductors to ensure functionality during nuclear or electromagnetic events. However, the high development cost of radiation-hardened technology is a key restraint, limiting adoption by smaller manufacturers. Despite this, significant opportunities exist. The rising use of autonomous vehicles is creating demand for radiation-hardened electronics to prevent malfunction in high-radiation areas, such as nuclear plants. Additionally, advancements in medical imaging technology are driving the need for radiation-resistant semiconductors in devices like CT scanners and radiotherapy equipment. For instance, SpaceX uses radiation-hardened microchips in its Starlink satellites to ensure durability in orbit. Similarly, in the defense sector, radiation-hardened processors are being integrated into fighter jets to enhance reliability during electronic warfare. As industries increasingly require durable and reliable electronics, the demand for radiation-hardened semiconductors is steadily growing, making them essential for mission-critical applications across space, defense, and medical sectors.

Driver: Space Missions Fueling Radiation-Hardened Demand

The growing demand for space exploration is significantly driving the need for radiation-hardened electronics and semiconductors. With more countries and private companies launching satellites, probes, and crewed missions, the importance of durable, radiation-resistant components is increasing. In space, electronics are constantly exposed to high levels of cosmic radiation, which can cause malfunctions or total system failure. Radiation-hardened semiconductors ensure stable performance in these harsh conditions. For example, NASA’s Mars rovers use radiation-resistant processors to withstand the planet’s radiation-rich environment, ensuring consistent functionality during long-term missions. Similarly, the European Space Agency (ESA) equips its satellites with radiation-hardened memory chips to prevent data corruption caused by cosmic rays. The rising trend of mega-constellations, where hundreds of satellites are launched for global communication networks, is further boosting the adoption of radiation-hardened technology. Companies developing lunar and Mars exploration vehicles are also investing in radiation-resistant electronics to enhance reliability. As space missions become more complex and frequent, the need for robust, radiation-tolerant components is expected to grow, making them essential for the long-term success and safety of space exploration endeavors.

Key Insights:

- The adoption rate of data center racks among IT and telecom industries is approximately 75%.

- In 2023, the total investment in data center infrastructure by the Indian government reached around USD 2.5 billion.

- The number of data center rack units sold globally in 2024 was estimated at 1.2 million units.

- The penetration rate of data center racks in the healthcare sector is about 65%.

- In 2024, investments from AWS in India's cloud infrastructure were projected to total USD 12.7 billion by 2030.

- The average annual growth rate of industrial racking systems in logistics and warehousing sectors is around 8.9%.

- The number of data centers in North America increased by approximately 10% from 2023 to 2024, reflecting a growing demand for rack solutions.

- The government initiatives aimed at enhancing digital infrastructure have led to a projected increase in data center capacity by over 50% by 2026.

Segment Analysis:

The global radiation-hardened electronics and semiconductors market is segmented by type and application, catering to specialized industries. Processors and controllers are widely used in spacecraft and defense systems, ensuring reliable data processing in high-radiation environments. For instance, radiation-hardened processors are integrated into military drones to maintain stable navigation during electronic warfare. Logic devices play a key role in managing control functions and signal processing in space applications. Satellites, for example, use radiation-hardened logic chips to ensure uninterrupted communication with ground stations. Memory components are essential for data storage in harsh conditions. Radiation-resistant memory is used in deep-space probes to prevent data corruption during long missions. Power management devices are crucial for regulating voltage and preventing radiation-induced malfunctions in sensitive equipment. In defense, radar systems use radiation-hardened power regulators to ensure consistent performance. ASICs (Application-Specific Integrated Circuits) are customized for mission-critical operations, such as in missile guidance systems, where precision and reliability are vital. On the application side, the aerospace and defense sector heavily relies on radiation-hardened electronics for secure communication, navigation, and weapon systems. In space, these components are essential for satellites, rovers, and telescopes, ensuring they remain operational despite constant exposure to cosmic radiation.

Regional Analysis:

The global radiation-hardened electronics and semiconductors market is expanding across regions, driven by increasing investments in space and defense programs. North America leads the market due to heavy government funding in military and space exploration. The U.S. Department of Defense uses radiation-hardened microcontrollers in missile defense systems to ensure functionality during nuclear events. In Europe, growing collaboration between space agencies and private firms is boosting demand. For instance, radiation-resistant semiconductors are used in ESA’s Earth observation satellites to prevent data loss during solar storms. The Asia-Pacific region is witnessing rapid growth due to rising space missions and military advancements. China uses radiation-hardened processors in its lunar exploration vehicles to withstand cosmic radiation. In Latin America, the growing adoption of satellite technology for communication and weather monitoring is driving the demand for durable electronics. For example, Brazil’s meteorological satellites use radiation-tolerant memory chips to ensure continuous data transmission. In the Middle East and Africa, increasing defense modernization is driving demand. Radiation-hardened components are used in advanced fighter jets and missile systems to enhance operational reliability. As nations strengthen their space and defense capabilities, the demand for radiation-hardened electronics is steadily rising across all regions.

Competitive Scenario:

Leading companies in the global radiation-hardened electronics and semiconductors market are driving growth through technological advancements, partnerships, and product innovation. Honeywell Aerospace is expanding its radiation-hardened product line by developing robust processors for space exploration missions, ensuring reliability in harsh environments. BAE Systems is enhancing its defense portfolio by introducing next-generation radiation-tolerant microelectronics for military satellites and weapon systems. Microsemi Corporation is focusing on radiation-hardened FPGAs (Field-Programmable Gate Arrays) to support high-performance computing in space applications. Xilinx Incorporation is advancing its programmable chips with radiation-hardened capabilities, making them ideal for satellite communication systems. Texas Instruments is developing radiation-resistant power management devices, ensuring stable performance in defense and aerospace equipment. Maxwell Technologies is innovating with radiation-tolerant energy storage solutions, enhancing reliability for space missions. Intersil Corporation is introducing advanced radiation-hardened voltage regulators to prevent power fluctuations in spacecraft. Atmel Corporation is expanding its radiation-resistant microcontroller range, catering to the growing demand in military-grade navigation systems. Linear Technology Corporation is developing radiation-hardened data converters for satellite imaging systems, ensuring accurate data capture. ST Microelectronics is investing in new radiation-hardened memory chips designed for deep-space probes, preventing data corruption. As companies prioritize innovation, the market continues to grow with increasingly advanced and durable solutions.

Radiation Hardened Electronics and Semiconductors Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 2.55 Billion |

| Revenue Forecast in 2035 | USD 8.84 Billion |

| Growth Rate | CAGR of 11.94% from 2025 to 2035 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2035 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | Honeywell Aerospace; BAE Systems; Microsemi Corporation; Xilinx Incorporation; Texas Instruments; Maxwell Technologies; Intersil Corporation; Atmel Corporation; Linear Technology Corporation; ST Microelectronics |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Radiation Hardened Electronics and Semiconductors Market report is segmented as follows:

By Type,

- Processors & Controllers

- Logic

- Memory

- Power Management

- ASICs

By Application,

- Aerospace & Defense

- Space

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East and Africa

Key Market Players,

- Honeywell Aerospace

- BAE Systems

- Microsemi Corporation

- Xilinx Incorporation

- Texas Instruments

- Maxwell Technologies

- Intersil Corporation

- Atmel Corporation

- Linear Technology Corporation

- ST Microelectronics

Frequently Asked Questions

Research Objectives

- Proliferation and maturation of trade in the global Radiation Hardened Electronics and Semiconductors Market.

- The market share of the global Radiation Hardened Electronics and Semiconductors Market, supply and demand ratio, growth revenue, supply chain analysis, and business overview.

- Current and future market trends that are influencing the growth opportunities and growth rate of the global Radiation Hardened Electronics and Semiconductors Market.

- Feasibility study, new market insights, company profiles, investment return, market size of the global Radiation Hardened Electronics and Semiconductors Market.

Chapter 1 Radiation Hardened Electronics and Semiconductors Market Executive Summary

- 1.1 Radiation Hardened Electronics and Semiconductors Market Research Scope

- 1.2 Radiation Hardened Electronics and Semiconductors Market Estimates and Forecast (2021-2035)

- 1.2.1 Global Radiation Hardened Electronics and Semiconductors Market Value and Growth Rate (2021-2035)

- 1.2.2 Global Radiation Hardened Electronics and Semiconductors Market Price Trend (2021-2035)

- 1.3 Global Radiation Hardened Electronics and Semiconductors Market Value Comparison, by Type (2021-2035)

- 1.3.1 Processors & Controllers

- 1.3.2 Logic

- 1.3.3 Memory

- 1.3.4 Power Management

- 1.3.5 ASICs

- 1.4 Global Radiation Hardened Electronics and Semiconductors Market Value Comparison, by Application (2021-2035)

- 1.4.1 Aerospace & Defense

- 1.4.2 Space

Chapter 2 Research Methodology

- 2.1 Introduction

- 2.2 Data Capture Sources

- 2.2.1 Primary Sources

- 2.2.2 Secondary Sources

- 2.3 Market Size Estimation

- 2.4 Market Forecast

- 2.5 Assumptions and Limitations

Chapter 3 Market Dynamics

- 3.1 Market Trends

- 3.2 Opportunities and Drivers

- 3.3 Challenges

- 3.4 Market Restraints

- 3.5 Porter's Five Forces Analysis

Chapter 4 Supply Chain Analysis and Marketing Channels

- 4.1 Radiation Hardened Electronics and Semiconductors Supply Chain Analysis

- 4.2 Marketing Channels

- 4.3 Radiation Hardened Electronics and Semiconductors Suppliers List

- 4.4 Radiation Hardened Electronics and Semiconductors Distributors List

- 4.5 Radiation Hardened Electronics and Semiconductors Customers

Chapter 5 COVID-19 & Russia?Ukraine War Impact Analysis

- 5.1 COVID-19 Impact Analysis on Radiation Hardened Electronics and Semiconductors Market

- 5.2 Russia-Ukraine War Impact Analysis on Radiation Hardened Electronics and Semiconductors Market

Chapter 6 Radiation Hardened Electronics and Semiconductors Market Estimate and Forecast by Region

- 6.1 Global Radiation Hardened Electronics and Semiconductors Market Value by Region: 2021 VS 2023 VS 2035

- 6.2 Global Radiation Hardened Electronics and Semiconductors Market Scenario by Region (2021-2023)

- 6.2.1 Global Radiation Hardened Electronics and Semiconductors Market Value Share by Region (2021-2023)

- 6.3 Global Radiation Hardened Electronics and Semiconductors Market Forecast by Region (2024-2035)

- 6.3.1 Global Radiation Hardened Electronics and Semiconductors Market Value Forecast by Region (2024-2035)

- 6.4 Geographic Market Analysis: Market Facts and Figures

- 6.4.1 North America Radiation Hardened Electronics and Semiconductors Market Estimates and Projections (2021-2035)

- 6.4.2 Europe Radiation Hardened Electronics and Semiconductors Market Estimates and Projections (2021-2035)

- 6.4.3 Asia Pacific Radiation Hardened Electronics and Semiconductors Market Estimates and Projections (2021-2035)

- 6.4.4 Latin America Radiation Hardened Electronics and Semiconductors Market Estimates and Projections (2021-2035)

- 6.4.5 Middle East & Africa Radiation Hardened Electronics and Semiconductors Market Estimates and Projections (2021-2035)

Chapter 7 Global Radiation Hardened Electronics and Semiconductors Competition Landscape by Players

- 7.1 Global Top Radiation Hardened Electronics and Semiconductors Players by Value (2021-2023)

- 7.2 Radiation Hardened Electronics and Semiconductors Headquarters and Sales Region by Company

- 7.3 Company Recent Developments, Mergers & Acquisitions, and Expansion Plans

Chapter 8 Global Radiation Hardened Electronics and Semiconductors Market, by Type

- 8.1 Global Radiation Hardened Electronics and Semiconductors Market Value, by Type (2021-2035)

- 8.1.1 Processors & Controllers

- 8.1.2 Logic

- 8.1.3 Memory

- 8.1.4 Power Management

- 8.1.5 ASICs

Chapter 9 Global Radiation Hardened Electronics and Semiconductors Market, by Application

- 9.1 Global Radiation Hardened Electronics and Semiconductors Market Value, by Application (2021-2035)

- 9.1.1 Aerospace & Defense

- 9.1.2 Space

Chapter 10 North America Radiation Hardened Electronics and Semiconductors Market

- 10.1 Overview

- 10.2 North America Radiation Hardened Electronics and Semiconductors Market Value, by Country (2021-2035)

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 North America Radiation Hardened Electronics and Semiconductors Market Value, by Type (2021-2035)

- 10.3.1 Processors & Controllers

- 10.3.2 Logic

- 10.3.3 Memory

- 10.3.4 Power Management

- 10.3.5 ASICs

- 10.4 North America Radiation Hardened Electronics and Semiconductors Market Value, by Application (2021-2035)

- 10.4.1 Aerospace & Defense

- 10.4.2 Space

Chapter 11 Europe Radiation Hardened Electronics and Semiconductors Market

- 11.1 Overview

- 11.2 Europe Radiation Hardened Electronics and Semiconductors Market Value, by Country (2021-2035)

- 11.2.1 UK

- 11.2.2 Germany

- 11.2.3 France

- 11.2.4 Spain

- 11.2.5 Italy

- 11.2.6 Russia

- 11.2.7 Rest of Europe

- 11.3 Europe Radiation Hardened Electronics and Semiconductors Market Value, by Type (2021-2035)

- 11.3.1 Processors & Controllers

- 11.3.2 Logic

- 11.3.3 Memory

- 11.3.4 Power Management

- 11.3.5 ASICs

- 11.4 Europe Radiation Hardened Electronics and Semiconductors Market Value, by Application (2021-2035)

- 11.4.1 Aerospace & Defense

- 11.4.2 Space

Chapter 12 Asia Pacific Radiation Hardened Electronics and Semiconductors Market

- 12.1 Overview

- 12.2 Asia Pacific Radiation Hardened Electronics and Semiconductors Market Value, by Country (2021-2035)

- 12.2.1 China

- 12.2.2 Japan

- 12.2.3 India

- 12.2.4 South Korea

- 12.2.5 Australia

- 12.2.6 Southeast Asia

- 12.2.7 Rest of Asia Pacific

- 12.3 Asia Pacific Radiation Hardened Electronics and Semiconductors Market Value, by Type (2021-2035)

- 12.3.1 Processors & Controllers

- 12.3.2 Logic

- 12.3.3 Memory

- 12.3.4 Power Management

- 12.3.5 ASICs

- 12.4 Asia Pacific Radiation Hardened Electronics and Semiconductors Market Value, by Application (2021-2035)

- 12.4.1 Aerospace & Defense

- 12.4.2 Space

Chapter 13 Latin America Radiation Hardened Electronics and Semiconductors Market

- 13.1 Overview

- 13.2 Latin America Radiation Hardened Electronics and Semiconductors Market Value, by Country (2021-2035)

- 13.2.1 Brazil

- 13.2.2 Argentina

- 13.2.3 Rest of Latin America

- 13.3 Latin America Radiation Hardened Electronics and Semiconductors Market Value, by Type (2021-2035)

- 13.3.1 Processors & Controllers

- 13.3.2 Logic

- 13.3.3 Memory

- 13.3.4 Power Management

- 13.3.5 ASICs

- 13.4 Latin America Radiation Hardened Electronics and Semiconductors Market Value, by Application (2021-2035)

- 13.4.1 Aerospace & Defense

- 13.4.2 Space

Chapter 14 Middle East & Africa Radiation Hardened Electronics and Semiconductors Market

- 14.1 Overview

- 14.2 Middle East & Africa Radiation Hardened Electronics and Semiconductors Market Value, by Country (2021-2035)

- 14.2.1 Saudi Arabia

- 14.2.2 UAE

- 14.2.3 South Africa

- 14.2.4 Rest of Middle East & Africa

- 14.3 Middle East & Africa Radiation Hardened Electronics and Semiconductors Market Value, by Type (2021-2035)

- 14.3.1 Processors & Controllers

- 14.3.2 Logic

- 14.3.3 Memory

- 14.3.4 Power Management

- 14.3.5 ASICs

- 14.4 Middle East & Africa Radiation Hardened Electronics and Semiconductors Market Value, by Application (2021-2035)

- 14.4.1 Aerospace & Defense

- 14.4.2 Space

Chapter 15 Company Profiles and Market Share Analysis: (Business Overview, Market Share Analysis, Products/Services Offered, Recent Developments)

- 15.1 Honeywell Aerospace

- 15.2 BAE Systems

- 15.3 Microsemi Corporation

- 15.4 Xilinx Incorporation

- 15.5 Texas Instruments

- 15.6 Maxwell Technologies

- 15.7 Intersil Corporation

- 15.8 Atmel Corporation

- 15.9 Linear Technology Corporation

- 15.10 ST Microelectronics

Related Reports

Report ID:

103

Published Date:

March 2025

Trusted by more than 10,500 organizations globally

Infaluble Methodology

Customization

Analyst Support

Targeted Market View