Global Modular Instruments Market, By Platform (PXI and PXIE, Benchtop, 19 Inch, VXI), By Distribution Channel, By End Use, and By Region - Trends and Forecast Analysis, 2021-2033

Publish Date: 2025-03-04 | Format: PDF | Category: Electronic and Semiconductor | Pages: 314

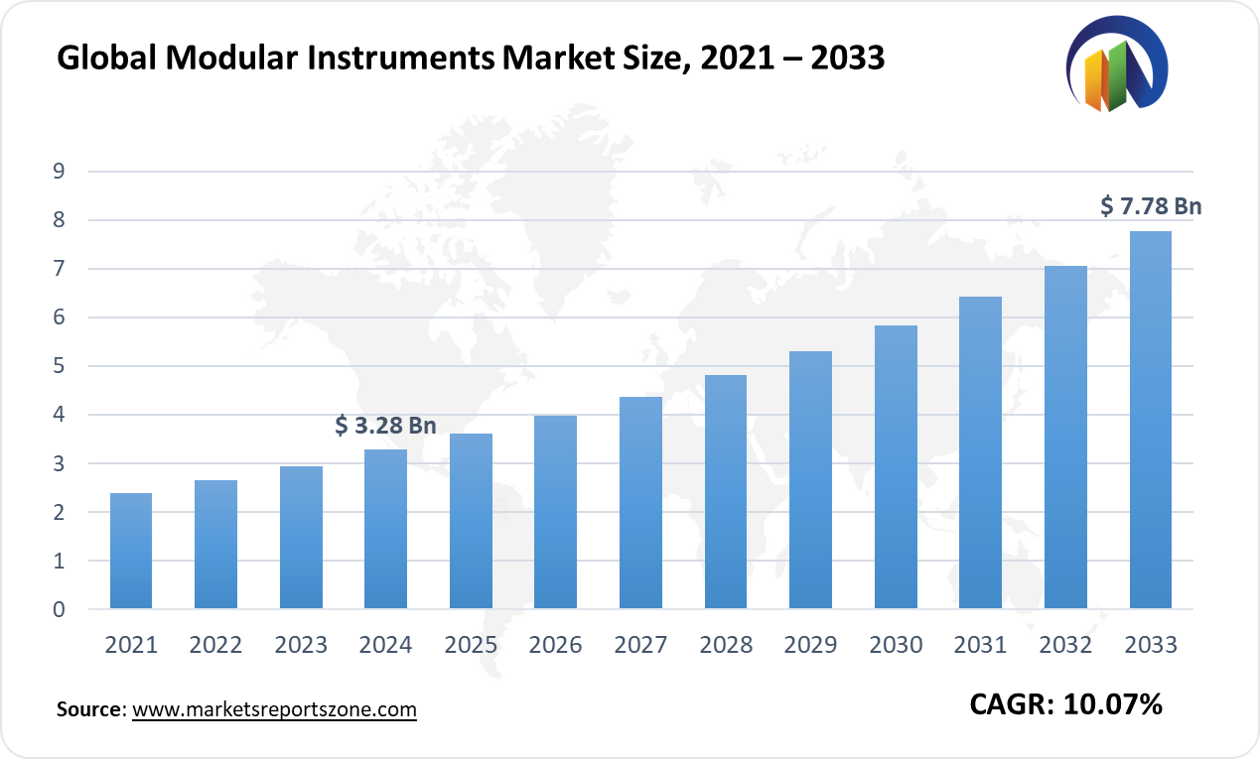

The Global Modular Instruments Market was valued at USD 3.28 Billion in 2024 and is projected to reach USD 7.78 Billion by 2033 at a CAGR of around 10.07% between 2024 and 2033. The global modular instruments market is driven by rising demand for flexible testing solutions and rapid advancements in wireless communication. Industries seek scalable and cost-effective instruments for diverse applications. The shift towards 5G and IoT has accelerated adoption. Complex electronic devices require precise testing, increasing demand. However, high initial costs act as a major restraint. Many small enterprises face budget constraints, limiting widespread adoption. Despite this, opportunities exist in the automotive sector, where EV testing is gaining traction. Modular instruments enable efficient validation of battery management systems. Another opportunity is seen in aerospace and defense.

Advanced radar and satellite communication systems demand adaptable testing solutions. Real-life examples highlight the market’s significance. In telecom, companies deploy modular instruments for network testing. The automotive industry integrates these for ADAS validation. Space agencies rely on them for satellite component verification. The growing reliance on AI and machine learning further enhances their utility. Remote monitoring and predictive maintenance benefit from modular testing setups. The evolving semiconductor industry also fuels demand. Manufacturers require high-precision testing for advanced chip designs. The market’s expansion is expected, driven by innovation. Increasing R&D investments and strategic collaborations shape future trends.

Driver: Rising Wireless Demand Boosts Growth

The increasing adoption of wireless technologies has fueled the demand for modular instruments. Industries rely on seamless connectivity, driving the need for efficient testing solutions. The shift towards Wi-Fi 6, 5G, and ultra-wideband networks has made traditional testing methods inefficient. Modular instruments offer flexibility and scalability, making them ideal for rapidly evolving wireless standards. Consumer electronics manufacturers use them to test smartphones, wearables, and smart home devices. In healthcare, wireless medical devices like remote monitoring systems require rigorous validation. Companies use modular instruments to ensure seamless data transmission.

The industrial sector also benefits, as smart factories implement IoT-driven automation. Wireless sensors and robotics depend on reliable connectivity, necessitating accurate testing. In aviation, next-generation communication systems for aircraft undergo extensive testing using modular setups. Even the entertainment industry sees their impact. Streaming services and cloud gaming platforms test network performance with these instruments. The automotive sector also embraces this trend. Connected cars require wireless communication validation for real-time navigation and safety features. As technology advances, the demand for adaptable and efficient testing solutions rises. Modular instruments are set to play a crucial role in shaping the future of wireless innovation across multiple industries.

Key Insights:

- The adoption of modular instruments in the semiconductor industry is increasing, with over 70% of manufacturers integrating them into their production lines.

- The U.S. Department of Defense has invested over $1 billion in modular testing equipment for advanced defense systems.

- Major companies like Keysight Technologies have reported selling over 100,000 modular instrument units annually.

- Modular instruments have achieved a penetration rate of about 40% in the telecommunications sector for network testing.

- The Indian government has allocated $500 million for setting up 5G testing labs, which heavily rely on modular instruments.

- Over 80% of automotive manufacturers use modular instruments for testing autonomous vehicle systems.

- Modular instruments are being integrated with AI in over 60% of new product developments in the aerospace sector.

- The Asia-Pacific region accounts for over 50% of the global demand for modular instruments due to rapid industrialization.

Segment Analysis:

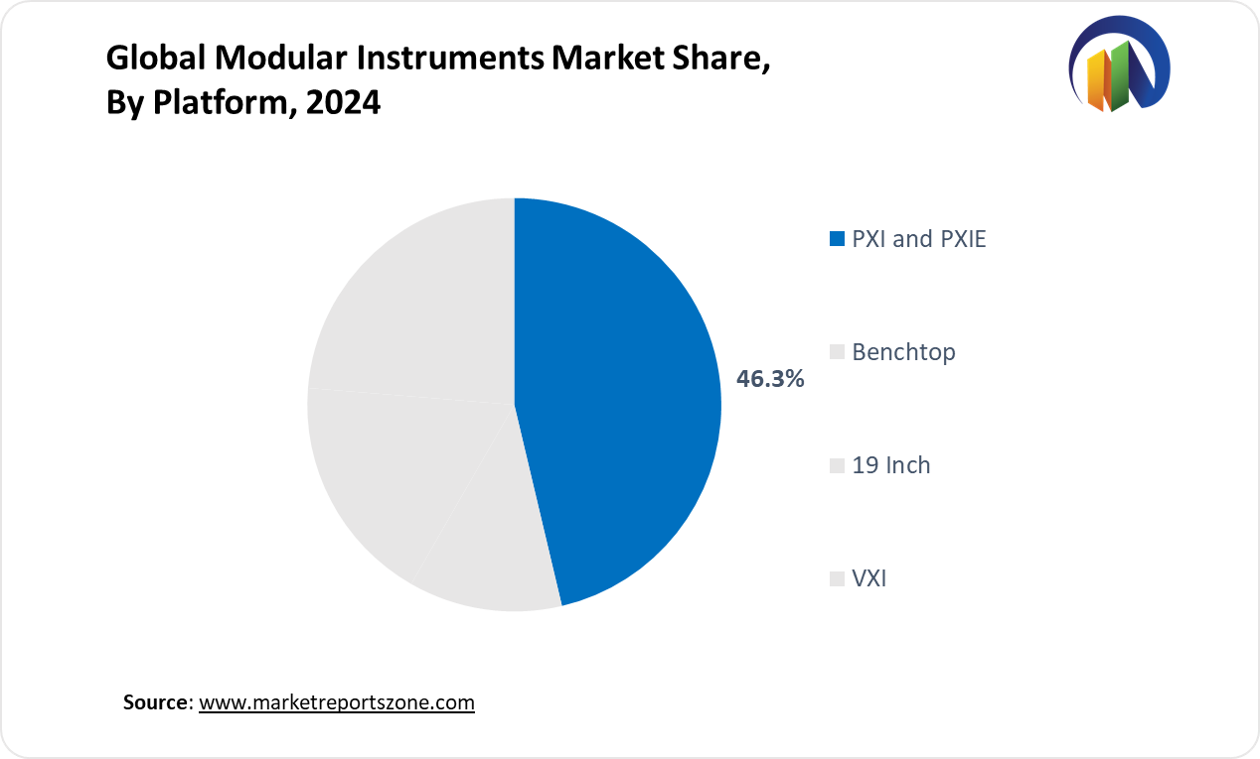

The modular instruments market is segmented by platform, distribution channel, and end use, each playing a crucial role in industry adoption. PXI and PXIe platforms are widely used due to their flexibility in automated testing, making them ideal for semiconductor validation. Benchtop instruments remain popular in R&D labs for quick prototype testing. The 19-inch form factor is commonly found in industrial applications, while VXI systems are preferred in military and aerospace testing due to their rugged design. Distribution channels include direct and indirect methods. Large enterprises prefer direct procurement for customized solutions, while smaller firms rely on distributors for cost-effective options. In end-use industries, telecommunications companies use modular instruments for network optimization and 5G infrastructure testing. Aerospace and defense sectors employ them for radar system evaluation and avionics testing. Automotive manufacturers leverage these instruments for electric vehicle powertrain validation. The transportation industry uses them for railway signaling system checks. In electronics and semiconductors, modular instruments ensure precise component quality control. Real-world applications include smartphone manufacturers using PXI-based setups for signal testing, satellite companies employing VXI for deep-space communication trials, and railway networks using benchtop instruments to validate automated track control systems, driving efficiency and innovation across industries.

Regional Analysis:

North America's modular instruments market is driven by strong aerospace and defense investments. Advanced radar and satellite communication systems rely on modular testing for precision. In Europe, the automotive industry plays a key role, with companies testing autonomous vehicle sensors using modular instruments. The Asia-Pacific region sees rapid growth due to rising electronics manufacturing, with companies testing consumer electronics like smartphones and laptops for performance and durability. In Latin America, industrial automation is boosting demand, as manufacturers use modular instruments for real-time equipment monitoring in production lines.

The Middle East & Africa region benefits from oil and gas sector advancements, where modular instruments help in pipeline diagnostics and refinery process optimization. Despite regional differences, technological advancements and increasing R&D investments fuel market expansion worldwide. Companies in North America focus on high-frequency testing for next-gen communication, while European firms emphasize sustainable automotive solutions. Asian manufacturers push for miniaturization in electronics, whereas Latin American industries aim for cost-effective automation. In the Middle East and Africa, energy firms optimize resource extraction with modular instruments. As industries evolve, modular instruments continue enhancing testing accuracy, efficiency, and innovation across global markets, ensuring technological advancements in multiple sectors worldwide.

Competitive Scenario:

The modular instruments market sees strong contributions from key players advancing testing and measurement technologies. Companies like Agilent Technologies, Keysight Technologies, and Rohde & Schwarz focus on high-frequency testing solutions for 5G, aerospace, and defense applications. Advantest Corporation and Teradyne Inc. drive semiconductor testing innovations, supporting chip manufacturers in ensuring performance and reliability. AMETEK, Inc. and Teledyne Technologies expand into precision instruments for industrial and scientific applications, enhancing automation and research capabilities. Astronics Corporation develops advanced test solutions for the aviation and space sectors, ensuring safety and efficiency.

Delta Electronics and Yokogawa Electric Corporation integrate modular instruments into power and energy management, optimizing smart grid systems. Pickering and Picotest Corp improve electronic design testing, catering to R&D needs. Thermo Fisher Scientific strengthens its position in life sciences by incorporating modular instruments into laboratory analysis. VIAVI Solutions Inc. advances network testing, supporting telecom infrastructure with real-time diagnostics. Fortive Corporation focuses on industrial automation, while recent developments include AI-driven testing tools, cloud-based modular platforms, and enhanced data analytics integration. Companies continue innovating to meet industry demands, improving efficiency, accuracy, and adaptability in testing solutions across telecommunications, semiconductors, aerospace, healthcare, and energy sectors.

Modular Instruments Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 3.28 Billion |

| Revenue Forecast in 2033 | USD 7.78 Billion |

| Growth Rate | CAGR of 10.07% from 2025 to 2033 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2033 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | Agilent Technologies; Advantest Corporation; AMETEK, Inc.; Astronics Corporation; Delta Electronics, Inc.; Fortive Corporation; Keysight Technologies; Picotest Corp Pickering, Rohde & Schwarz, Thermo Fisher Scientific, Teledyne Technologies Incorporated, Teradyne Inc, VIAVI Solutions Inc., Yokogawa Electric Corporation; Others |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Modular Instruments Market report is segmented as follows:

By Platform,

- PXI and PXIE

- Benchtop

- 19 Inch

- VXI

By Distribution Channel,

- Direct Distribution

- Indirect Distribution

- Others

By End Use,

- Telecommunications

- Aerospace & Defense

- Automotive

- Transportation

- Electronics

- Semiconductor

- Others

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East & Africa

Key Market Players,

- Agilent Technologies

- Advantest Corporation

- AMETEK, Inc.

- Astronics Corporation

- Delta Electronics, Inc.

- Fortive Corporation

- Keysight Technologies

- Picotest Corp Pickering, Rohde & Schwarz, Thermo Fisher Scientific, Teledyne Technologies Incorporated, Teradyne Inc, VIAVI Solutions Inc., Yokogawa Electric Corporation

- Others

Frequently Asked Questions

Research Objectives

- Proliferation and maturation of trade in the global Modular Instruments Market.

- The market share of the global Modular Instruments Market, supply and demand ratio, growth revenue, supply chain analysis, and business overview.

- Current and future market trends that are influencing the growth opportunities and growth rate of the global Modular Instruments Market.

- Feasibility study, new market insights, company profiles, investment return, market size of the global Modular Instruments Market.

Chapter 1 Modular Instruments Market Executive Summary

- 1.1 Modular Instruments Market Research Scope

- 1.2 Modular Instruments Market Estimates and Forecast (2021-2033)

- 1.2.1 Global Modular Instruments Market Value and Volume and Growth Rate (2021-2033)

- 1.2.2 Global Modular Instruments Market Price Trend (2021-2033)

- 1.3 Global Modular Instruments Market Value and Volume Comparison, by Platform (2021-2033)

- 1.3.1 PXI and PXIE

- 1.3.2 Benchtop

- 1.3.3 19 Inch

- 1.3.4 VXI

- 1.4 Global Modular Instruments Market Value and Volume Comparison, by Distribution Channel (2021-2033)

- 1.4.1 Direct Distribution

- 1.4.2 Indirect Distribution

- 1.4.3 Others

- 1.5 Global Modular Instruments Market Value and Volume Comparison, by End Use (2021-2033)

- 1.5.1 Telecommunications

- 1.5.2 Aerospace & Defense

- 1.5.3 Automotive

- 1.5.4 Transportation

- 1.5.5 Electronics

- 1.5.6 Semiconductor

- 1.5.7 Others

Chapter 2 Research Methodology

- 2.1 Introduction

- 2.2 Data Capture Sources

- 2.2.1 Primary Sources

- 2.2.2 Secondary Sources

- 2.3 Market Size Estimation

- 2.4 Market Forecast

- 2.5 Assumptions and Limitations

Chapter 3 Market Dynamics

- 3.1 Market Trends

- 3.2 Opportunities and Drivers

- 3.3 Challenges

- 3.4 Market Restraints

- 3.5 Porter's Five Forces Analysis

Chapter 4 Supply Chain Analysis and Marketing Channels

- 4.1 Modular Instruments Supply Chain Analysis

- 4.2 Marketing Channels

- 4.3 Modular Instruments Suppliers List

- 4.4 Modular Instruments Distributors List

- 4.5 Modular Instruments Customers

Chapter 5 COVID-19 & Russia–Ukraine War Impact Analysis

- 5.1 COVID-19 Impact Analysis on Modular Instruments Market

- 5.2 Russia-Ukraine War Impact Analysis on Modular Instruments Market

Chapter 6 Modular Instruments Market Estimate and Forecast by Region

- 6.1 Global Modular Instruments Market Value by Region: 2021 VS 2023 VS 2033

- 6.2 Global Modular Instruments Market Scenario by Region (2021-2023)

- 6.2.1 Global Modular Instruments Market Value and Volume Share by Region (2021-2023)

- 6.3 Global Modular Instruments Market Forecast by Region (2024-2033)

- 6.3.1 Global Modular Instruments Market Value and Volume Forecast by Region (2024-2033)

- 6.4 Geographic Market Analysis: Market Facts and Figures

- 6.4.1 North America Modular Instruments Market Estimates and Projections (2021-2033)

- 6.4.2 Europe Modular Instruments Market Estimates and Projections (2021-2033)

- 6.4.3 Asia Pacific Modular Instruments Market Estimates and Projections (2021-2033)

- 6.4.4 Latin America Modular Instruments Market Estimates and Projections (2021-2033)

- 6.4.5 Middle East & Africa Modular Instruments Market Estimates and Projections (2021-2033)

Chapter 7 Global Modular Instruments Competition Landscape by Players

- 7.1 Global Top Modular Instruments Players by Value (2021-2023)

- 7.2 Modular Instruments Headquarters and Sales Region by Company

- 7.3 Company Recent Developments, Mergers & Acquisitions, and Expansion Plans

Chapter 8 Global Modular Instruments Market, by Platform

- 8.1 Global Modular Instruments Market Value and Volume, by Platform (2021-2033)

- 8.1.1 PXI and PXIE

- 8.1.2 Benchtop

- 8.1.3 19 Inch

- 8.1.4 VXI

Chapter 9 Global Modular Instruments Market, by Distribution Channel

- 9.1 Global Modular Instruments Market Value and Volume, by Distribution Channel (2021-2033)

- 9.1.1 Direct Distribution

- 9.1.2 Indirect Distribution

- 9.1.3 Others

Chapter 10 Global Modular Instruments Market, by End Use

- 10.1 Global Modular Instruments Market Value and Volume, by End Use (2021-2033)

- 10.1.1 Telecommunications

- 10.1.2 Aerospace & Defense

- 10.1.3 Automotive

- 10.1.4 Transportation

- 10.1.5 Electronics

- 10.1.6 Semiconductor

- 10.1.7 Others

Chapter 11 North America Modular Instruments Market

- 11.1 Overview

- 11.2 North America Modular Instruments Market Value and Volume, by Country (2021-2033)

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 North America Modular Instruments Market Value and Volume, by Platform (2021-2033)

- 11.3.1 PXI and PXIE

- 11.3.2 Benchtop

- 11.3.3 19 Inch

- 11.3.4 VXI

- 11.4 North America Modular Instruments Market Value and Volume, by Distribution Channel (2021-2033)

- 11.4.1 Direct Distribution

- 11.4.2 Indirect Distribution

- 11.4.3 Others

- 11.5 North America Modular Instruments Market Value and Volume, by End Use (2021-2033)

- 11.5.1 Telecommunications

- 11.5.2 Aerospace & Defense

- 11.5.3 Automotive

- 11.5.4 Transportation

- 11.5.5 Electronics

- 11.5.6 Semiconductor

- 11.5.7 Others

Chapter 12 Europe Modular Instruments Market

- 12.1 Overview

- 12.2 Europe Modular Instruments Market Value and Volume, by Country (2021-2033)

- 12.2.1 UK

- 12.2.2 Germany

- 12.2.3 France

- 12.2.4 Spain

- 12.2.5 Italy

- 12.2.6 Russia

- 12.2.7 Rest of Europe

- 12.3 Europe Modular Instruments Market Value and Volume, by Platform (2021-2033)

- 12.3.1 PXI and PXIE

- 12.3.2 Benchtop

- 12.3.3 19 Inch

- 12.3.4 VXI

- 12.4 Europe Modular Instruments Market Value and Volume, by Distribution Channel (2021-2033)

- 12.4.1 Direct Distribution

- 12.4.2 Indirect Distribution

- 12.4.3 Others

- 12.5 Europe Modular Instruments Market Value and Volume, by End Use (2021-2033)

- 12.5.1 Telecommunications

- 12.5.2 Aerospace & Defense

- 12.5.3 Automotive

- 12.5.4 Transportation

- 12.5.5 Electronics

- 12.5.6 Semiconductor

- 12.5.7 Others

Chapter 13 Asia Pacific Modular Instruments Market

- 13.1 Overview

- 13.2 Asia Pacific Modular Instruments Market Value and Volume, by Country (2021-2033)

- 13.2.1 China

- 13.2.2 Japan

- 13.2.3 India

- 13.2.4 South Korea

- 13.2.5 Australia

- 13.2.6 Southeast Asia

- 13.2.7 Rest of Asia Pacific

- 13.3 Asia Pacific Modular Instruments Market Value and Volume, by Platform (2021-2033)

- 13.3.1 PXI and PXIE

- 13.3.2 Benchtop

- 13.3.3 19 Inch

- 13.3.4 VXI

- 13.4 Asia Pacific Modular Instruments Market Value and Volume, by Distribution Channel (2021-2033)

- 13.4.1 Direct Distribution

- 13.4.2 Indirect Distribution

- 13.4.3 Others

- 13.5 Asia Pacific Modular Instruments Market Value and Volume, by End Use (2021-2033)

- 13.5.1 Telecommunications

- 13.5.2 Aerospace & Defense

- 13.5.3 Automotive

- 13.5.4 Transportation

- 13.5.5 Electronics

- 13.5.6 Semiconductor

- 13.5.7 Others

Chapter 14 Latin America Modular Instruments Market

- 14.1 Overview

- 14.2 Latin America Modular Instruments Market Value and Volume, by Country (2021-2033)

- 14.2.1 Brazil

- 14.2.2 Argentina

- 14.2.3 Rest of Latin America

- 14.3 Latin America Modular Instruments Market Value and Volume, by Platform (2021-2033)

- 14.3.1 PXI and PXIE

- 14.3.2 Benchtop

- 14.3.3 19 Inch

- 14.3.4 VXI

- 14.4 Latin America Modular Instruments Market Value and Volume, by Distribution Channel (2021-2033)

- 14.4.1 Direct Distribution

- 14.4.2 Indirect Distribution

- 14.4.3 Others

- 14.5 Latin America Modular Instruments Market Value and Volume, by End Use (2021-2033)

- 14.5.1 Telecommunications

- 14.5.2 Aerospace & Defense

- 14.5.3 Automotive

- 14.5.4 Transportation

- 14.5.5 Electronics

- 14.5.6 Semiconductor

- 14.5.7 Others

Chapter 15 Middle East & Africa Modular Instruments Market

- 15.1 Overview

- 15.2 Middle East & Africa Modular Instruments Market Value and Volume, by Country (2021-2033)

- 15.2.1 Saudi Arabia

- 15.2.2 UAE

- 15.2.3 South Africa

- 15.2.4 Rest of Middle East & Africa

- 15.3 Middle East & Africa Modular Instruments Market Value and Volume, by Platform (2021-2033)

- 15.3.1 PXI and PXIE

- 15.3.2 Benchtop

- 15.3.3 19 Inch

- 15.3.4 VXI

- 15.4 Middle East & Africa Modular Instruments Market Value and Volume, by Distribution Channel (2021-2033)

- 15.4.1 Direct Distribution

- 15.4.2 Indirect Distribution

- 15.4.3 Others

- 15.5 Middle East & Africa Modular Instruments Market Value and Volume, by End Use (2021-2033)

- 15.5.1 Telecommunications

- 15.5.2 Aerospace & Defense

- 15.5.3 Automotive

- 15.5.4 Transportation

- 15.5.5 Electronics

- 15.5.6 Semiconductor

- 15.5.7 Others

Chapter 16 Company Profiles and Market Share Analysis: (Business Overview, Market Share Analysis, Products/Services Offered, Recent Developments)

- 16.1 Agilent Technologies

- 16.2 Advantest Corporation

- 16.3 AMETEK, Inc.

- 16.4 Astronics Corporation

- 16.5 Delta Electronics, Inc.

- 16.6 Fortive Corporation

- 16.7 Keysight Technologies

- 16.8 Picotest Corp Pickering, Rohde & Schwarz, Thermo Fisher Scientific, Teledyne Technologies Incorporated, Teradyne Inc, VIAVI Solutions Inc., Yokogawa Electric Corporation

- 16.9 Others

Report ID:

25

Published Date:

March 2025

Trusted by more than 10,500 organizations globally

Infaluble Methodology

Customization

Analyst Support

Targeted Market View