Global GNSS Device Market, By Technology (Satellite Navigation, Differential GNSS, Real-Time Kinematic), By Device Type, By Application, By End Use, and By Region - Trends and Forecast Analysis, 2021-2033

Publish Date: 2025-03-03 | Format: PDF | Category: ICT Media | Pages: 250

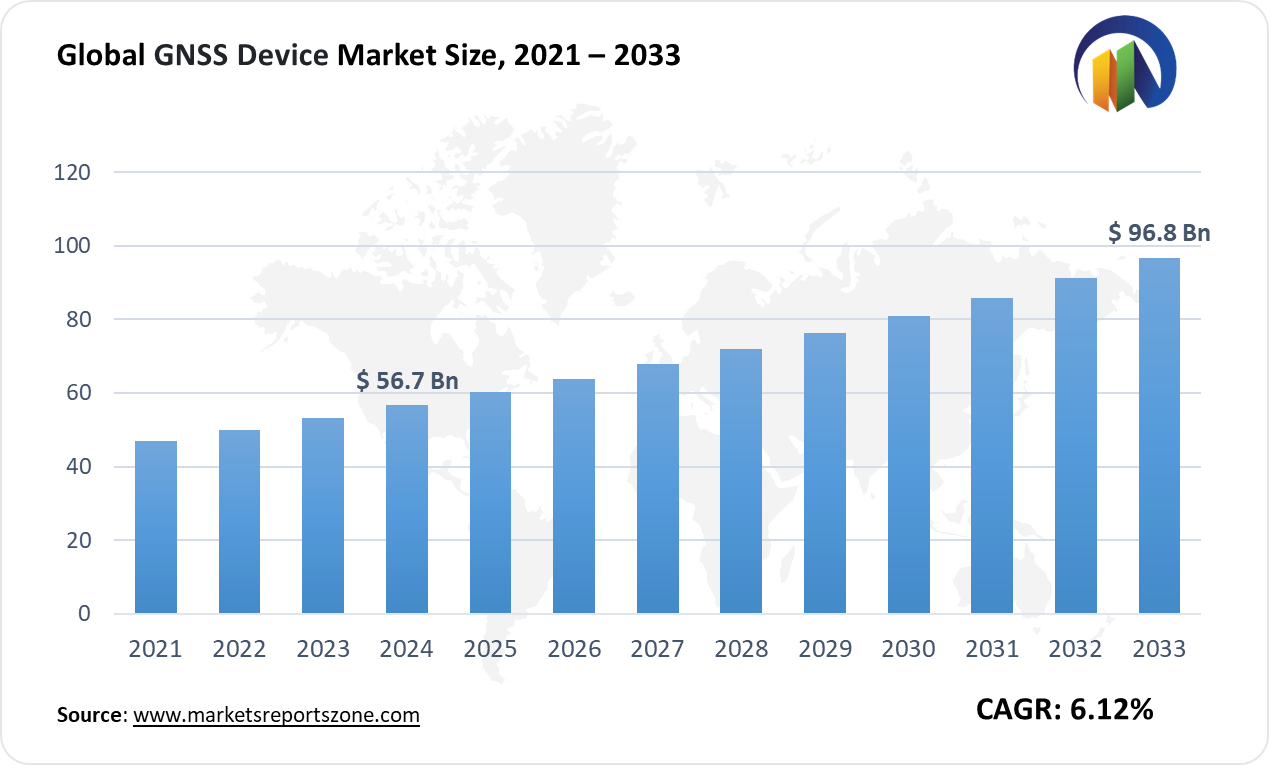

The Global GNSS Device Market was valued at USD 56.7 Billion in 2024 and is projected to reach USD 96.8 Billion by 2033 at a CAGR of around 6.12% between 2024 and 2033. The Global GNSS Device Market is driven by rising demand for navigation and positioning in automotive and consumer electronics. GNSS-enabled smartphones and in-car navigation systems are widely used. The expansion of IoT and smart city projects also boosts demand. Precise location tracking is required for fleet management and autonomous vehicles. However, high costs and signal obstructions in urban areas restrain market growth. Buildings and tunnels often disrupt signals, affecting accuracy. Despite this, significant opportunities exist. The integration of GNSS in agriculture improves productivity.

Farmers use GPS-guided tractors for precision farming. Another key opportunity lies in disaster management. GNSS aids emergency responders in locating affected areas quickly. Real-time tracking enhances rescue operations during earthquakes and floods. The market continues to evolve with technological advancements. GNSS applications are expanding in drones, aviation, and defense. Drones rely on GNSS for stable flights and accurate deliveries. Aviation safety also improves with satellite-based navigation systems. The growing adoption of wearable devices further fuels demand. Smartwatches and fitness trackers use GNSS for activity monitoring. This trend is increasing among health-conscious consumers. As innovations continue, GNSS technology remains essential across multiple sectors. Widespread applications ensure steady market expansion in the coming years.

Driver: Growing Demand for Smart Navigation

The increasing reliance on GNSS devices in daily life drives market growth. Modern transportation depends on precise navigation for efficiency and safety. Ride-hailing services use GNSS for accurate pick-ups and drop-offs. Drivers follow optimized routes to save time and fuel. Public transport systems also integrate GNSS for real-time tracking. Commuters check bus and train locations on mobile apps. Logistics companies use GNSS for shipment tracking. Customers monitor deliveries with live location updates. In aviation, pilots rely on GNSS for precise landing approaches. It enhances flight safety and reduces delays. Marine navigation has also transformed with satellite positioning. Cargo ships and fishing vessels depend on GNSS to navigate open waters. Emergency services benefit from accurate location tracking. Ambulances reach patients faster, improving survival chances.

Adventure enthusiasts use GNSS devices for trekking and cycling. Hikers follow mapped trails with confidence. Cyclists track routes and distances on GPS-enabled devices. Even pet owners use GNSS-powered trackers for lost pets. The growing need for seamless navigation fuels demand across industries. As more sectors adopt GNSS, its impact becomes even stronger. Enhanced accuracy and real-time location tracking ensure continued market expansion.

Key Insights:

- Over 95% of smartphones worldwide are now equipped with GNSS capabilities, enabling precise location tracking.

- The European Union has invested more than €10 billion in the Galileo satellite navigation system for enhanced global positioning.

- The U.S. government allocates approximately $1.8 billion annually for GPS system upgrades, maintenance, and modernization.

- China’s BeiDou Navigation Satellite System (BDS) has achieved over 85% penetration in industries such as transportation, logistics, and agriculture.

- More than 80% of new passenger vehicles come with built-in GNSS-based navigation and telematics systems for enhanced driving assistance.

- The drone industry relies on GNSS, with over 85% of commercial drones using satellite navigation for accurate flight control and mapping.

- Wearable GNSS device shipments exceeded 160 million units in a year, fueled by the growing demand for fitness tracking and outdoor navigation.

- GNSS-enabled fleet tracking systems have improved logistics efficiency by over 25%, reducing fuel costs and optimizing delivery routes.

Segment Analysis:

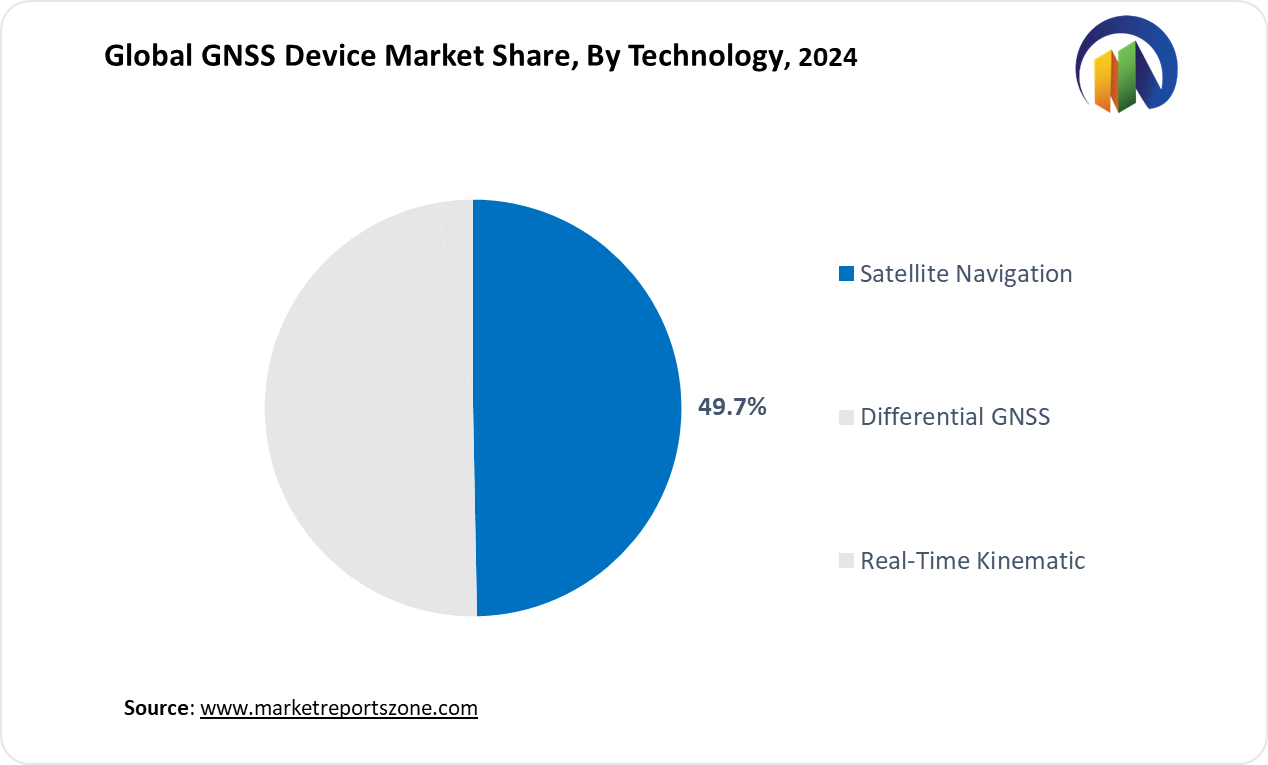

The GNSS device market is expanding across multiple segments with diverse applications. By technology, satellite navigation remains dominant, offering global coverage for travel and logistics. Differential GNSS enhances precision, benefiting land surveying and agriculture. Real-Time Kinematic (RTK) technology is widely used in construction, where bulldozers and excavators rely on centimeter-level accuracy. By device type, handheld GNSS receivers support outdoor activities like hiking and geocaching. OEM GNSS modules power advanced applications, including robotic automation in warehouses. Smartphone GNSS remains the most widely used, assisting commuters with real-time navigation and location-based services. By application, automotive integration is growing with connected car systems and autonomous driving.

Aerospace relies on GNSS for flight route optimization, while the marine sector uses it for cargo ship tracking and fishing vessel navigation. Telecommunication networks synchronize data transmission using precise GNSS timing. By end use, commercial adoption is expanding in ride-sharing services and fleet management. Personal use is rising, with pet tracking collars and smartwatches using GNSS. Industrial applications are advancing in mining, where autonomous haul trucks navigate using satellite guidance. The market’s growth is fueled by increasing dependence on accurate positioning across industries, ensuring efficiency, safety, and innovation in everyday operations.

Regional Analysis:

The GNSS device market is witnessing strong growth across all major regions, driven by increasing adoption in various industries. In North America, advanced transportation systems and defense applications rely heavily on GNSS. The rise of self-driving trucks and smart traffic management enhances efficiency. Farmers also use precision agriculture techniques, such as GPS-guided irrigation. In Europe, strong government investments in satellite navigation, such as Galileo, are driving innovation. The region’s aviation industry depends on GNSS for air traffic management, while rail networks use it for real-time train tracking. Asia-Pacific leads in consumer electronics, with widespread smartphone GNSS adoption.

Ride-hailing services in urban centers depend on accurate navigation. In India, GNSS is transforming railway safety by preventing collisions through satellite-based monitoring. In Latin America, GNSS is revolutionizing logistics and infrastructure. Delivery companies use location tracking to optimize routes, while maritime navigation benefits from satellite-based positioning for safer cargo shipments. In the Middle East & Africa, the technology supports desert navigation and oil exploration. Remote monitoring of pipelines reduces operational risks, while wildlife conservation efforts use GNSS to track endangered species. As GNSS applications expand, each region continues to develop localized solutions, enhancing efficiency across industries and everyday life.

Competition Landscape:

Leading companies in the GNSS device market are driving innovation with advanced solutions across industries. Hexagon and Trimble are expanding high-precision GNSS for surveying, construction, and agriculture. Their real-time kinematic (RTK) technology improves accuracy in land mapping and autonomous farming equipment. Rockwell Collins focuses on aerospace and defense, integrating GNSS into aircraft navigation and military-grade positioning systems. Garmin continues to dominate consumer and automotive segments with upgraded GPS wearables and in-car navigation systems. Qualcomm and Broadcom lead in smartphone GNSS technology, enhancing location accuracy for 5G-enabled devices. Magellan and TomTom remain strong in personal and automotive navigation, with AI-powered route optimization and real-time traffic updates.

Nokia and Huawei integrate GNSS into telecommunication infrastructure, improving network synchronization and IoT applications. Navcom Technology and Stonex specialize in industrial-grade GNSS for geospatial and marine navigation. Sony is advancing GNSS in camera technology, enabling precise geotagging for professional photography. Skyhook enhances Wi-Fi positioning with hybrid GNSS solutions for smart city applications. ublox is innovating in autonomous vehicle navigation with ultra-precise GNSS modules. These companies continue investing in satellite positioning advancements, ensuring higher accuracy, reliability, and expanded applications across industries. Their developments shape the future of connected and automated systems worldwide.

GNSS Device Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 56.7 Billion |

| Revenue Forecast in 2033 | USD 96.8 Billion |

| Growth Rate | CAGR of 6.12% from 2025 to 2033 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2033 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | Hexagon; Rockwell Collins; Trimble; Garmin; Qualcomm; Magellan; Nokia; Navcom Technology; Skyhook; Huawei; Sony; Stonex; TomTom; ublox; Broadcom; Others |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global GNSS Device Market report is segmented as follows:

By Technology,

- Satellite Navigation

- Differential GNSS

- Real-Time Kinematic

By Device Type,

- Handheld GNSS Receivers

- OEM GNSS Modules

- Smartphone GNSS

By Application,

- Automotive

- Aerospace

- Marine

- Telecommunication

By End Use,

- Commercial Use

- Personal Use

- Industrial Use

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East & Africa

Key Market Players,

- Hexagon

- Rockwell Collins

- Trimble

- Garmin

- Qualcomm

- Magellan

- Nokia

- Navcom Technology

- Skyhook

- Huawei

- Sony

- Stonex

- TomTom

- ublox

- Broadcom

- Others

Frequently Asked Questions

Research Objectives

- Proliferation and maturation of trade in the global GNSS Device Market.

- The market share of the global GNSS Device Market, supply and demand ratio, growth revenue, supply chain analysis, and business overview.

- Current and future market trends that are influencing the growth opportunities and growth rate of the global GNSS Device Market.

- Feasibility study, new market insights, company profiles, investment return, market size of the global GNSS Device Market.

Chapter 1 GNSS Device Market Executive Summary

- 1.1 GNSS Device Market Research Scope

- 1.2 GNSS Device Market Estimates and Forecast (2021-2033)

- 1.2.1 Global GNSS Device Market Value and Volume and Growth Rate (2021-2033)

- 1.2.2 Global GNSS Device Market Price Trend (2021-2033)

- 1.3 Global GNSS Device Market Value and Volume Comparison, by Technology (2021-2033)

- 1.3.1 Satellite Navigation

- 1.3.2 Differential GNSS

- 1.3.3 Real-Time Kinematic

- 1.4 Global GNSS Device Market Value and Volume Comparison, by Device Type (2021-2033)

- 1.4.1 Handheld GNSS Receivers

- 1.4.2 OEM GNSS Modules

- 1.4.3 Smartphone GNSS

- 1.5 Global GNSS Device Market Value and Volume Comparison, by Application (2021-2033)

- 1.5.1 Automotive

- 1.5.2 Aerospace

- 1.5.3 Marine

- 1.5.4 Telecommunication

- 1.6 Global GNSS Device Market Value and Volume Comparison, by End Use (2021-2033)

- 1.6.1 Commercial Use

- 1.6.2 Personal Use

- 1.6.3 Industrial Use

Chapter 2 Research Methodology

- 2.1 Introduction

- 2.2 Data Capture Sources

- 2.2.1 Primary Sources

- 2.2.2 Secondary Sources

- 2.3 Market Size Estimation

- 2.4 Market Forecast

- 2.5 Assumptions and Limitations

Chapter 3 Market Dynamics

- 3.1 Market Trends

- 3.2 Opportunities and Drivers

- 3.3 Challenges

- 3.4 Market Restraints

- 3.5 Porter's Five Forces Analysis

Chapter 4 Supply Chain Analysis and Marketing Channels

- 4.1 GNSS Device Supply Chain Analysis

- 4.2 Marketing Channels

- 4.3 GNSS Device Suppliers List

- 4.4 GNSS Device Distributors List

- 4.5 GNSS Device Customers

Chapter 5 COVID-19 & Russia–Ukraine War Impact Analysis

- 5.1 COVID-19 Impact Analysis on GNSS Device Market

- 5.2 Russia-Ukraine War Impact Analysis on GNSS Device Market

Chapter 6 GNSS Device Market Estimate and Forecast by Region

- 6.1 Global GNSS Device Market Value by Region: 2021 VS 2023 VS 2033

- 6.2 Global GNSS Device Market Scenario by Region (2021-2023)

- 6.2.1 Global GNSS Device Market Value and Volume Share by Region (2021-2023)

- 6.3 Global GNSS Device Market Forecast by Region (2024-2033)

- 6.3.1 Global GNSS Device Market Value and Volume Forecast by Region (2024-2033)

- 6.4 Geographic Market Analysis: Market Facts and Figures

- 6.4.1 North America GNSS Device Market Estimates and Projections (2021-2033)

- 6.4.2 Europe GNSS Device Market Estimates and Projections (2021-2033)

- 6.4.3 Asia Pacific GNSS Device Market Estimates and Projections (2021-2033)

- 6.4.4 Latin America GNSS Device Market Estimates and Projections (2021-2033)

- 6.4.5 Middle East & Africa GNSS Device Market Estimates and Projections (2021-2033)

Chapter 7 Global GNSS Device Competition Landscape by Players

- 7.1 Global Top GNSS Device Players by Value (2021-2023)

- 7.2 GNSS Device Headquarters and Sales Region by Company

- 7.3 Company Recent Developments, Mergers & Acquisitions, and Expansion Plans

Chapter 8 Global GNSS Device Market, by Technology

- 8.1 Global GNSS Device Market Value and Volume, by Technology (2021-2033)

- 8.1.1 Satellite Navigation

- 8.1.2 Differential GNSS

- 8.1.3 Real-Time Kinematic

Chapter 9 Global GNSS Device Market, by Device Type

- 9.1 Global GNSS Device Market Value and Volume, by Device Type (2021-2033)

- 9.1.1 Handheld GNSS Receivers

- 9.1.2 OEM GNSS Modules

- 9.1.3 Smartphone GNSS

Chapter 10 Global GNSS Device Market, by Application

- 10.1 Global GNSS Device Market Value and Volume, by Application (2021-2033)

- 10.1.1 Automotive

- 10.1.2 Aerospace

- 10.1.3 Marine

- 10.1.4 Telecommunication

Chapter 11 Global GNSS Device Market, by End Use

- 11.1 Global GNSS Device Market Value and Volume, by End Use (2021-2033)

- 11.1.1 Commercial Use

- 11.1.2 Personal Use

- 11.1.3 Industrial Use

Chapter 12 North America GNSS Device Market

- 12.1 Overview

- 12.2 North America GNSS Device Market Value and Volume, by Country (2021-2033)

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.2.3 Mexico

- 12.3 North America GNSS Device Market Value and Volume, by Technology (2021-2033)

- 12.3.1 Satellite Navigation

- 12.3.2 Differential GNSS

- 12.3.3 Real-Time Kinematic

- 12.4 North America GNSS Device Market Value and Volume, by Device Type (2021-2033)

- 12.4.1 Handheld GNSS Receivers

- 12.4.2 OEM GNSS Modules

- 12.4.3 Smartphone GNSS

- 12.5 North America GNSS Device Market Value and Volume, by Application (2021-2033)

- 12.5.1 Automotive

- 12.5.2 Aerospace

- 12.5.3 Marine

- 12.5.4 Telecommunication

- 12.6 North America GNSS Device Market Value and Volume, by End Use (2021-2033)

- 12.6.1 Commercial Use

- 12.6.2 Personal Use

- 12.6.3 Industrial Use

Chapter 13 Europe GNSS Device Market

- 13.1 Overview

- 13.2 Europe GNSS Device Market Value and Volume, by Country (2021-2033)

- 13.2.1 UK

- 13.2.2 Germany

- 13.2.3 France

- 13.2.4 Spain

- 13.2.5 Italy

- 13.2.6 Russia

- 13.2.7 Rest of Europe

- 13.3 Europe GNSS Device Market Value and Volume, by Technology (2021-2033)

- 13.3.1 Satellite Navigation

- 13.3.2 Differential GNSS

- 13.3.3 Real-Time Kinematic

- 13.4 Europe GNSS Device Market Value and Volume, by Device Type (2021-2033)

- 13.4.1 Handheld GNSS Receivers

- 13.4.2 OEM GNSS Modules

- 13.4.3 Smartphone GNSS

- 13.5 Europe GNSS Device Market Value and Volume, by Application (2021-2033)

- 13.5.1 Automotive

- 13.5.2 Aerospace

- 13.5.3 Marine

- 13.5.4 Telecommunication

- 13.6 Europe GNSS Device Market Value and Volume, by End Use (2021-2033)

- 13.6.1 Commercial Use

- 13.6.2 Personal Use

- 13.6.3 Industrial Use

Chapter 14 Asia Pacific GNSS Device Market

- 14.1 Overview

- 14.2 Asia Pacific GNSS Device Market Value and Volume, by Country (2021-2033)

- 14.2.1 China

- 14.2.2 Japan

- 14.2.3 India

- 14.2.4 South Korea

- 14.2.5 Australia

- 14.2.6 Southeast Asia

- 14.2.7 Rest of Asia Pacific

- 14.3 Asia Pacific GNSS Device Market Value and Volume, by Technology (2021-2033)

- 14.3.1 Satellite Navigation

- 14.3.2 Differential GNSS

- 14.3.3 Real-Time Kinematic

- 14.4 Asia Pacific GNSS Device Market Value and Volume, by Device Type (2021-2033)

- 14.4.1 Handheld GNSS Receivers

- 14.4.2 OEM GNSS Modules

- 14.4.3 Smartphone GNSS

- 14.5 Asia Pacific GNSS Device Market Value and Volume, by Application (2021-2033)

- 14.5.1 Automotive

- 14.5.2 Aerospace

- 14.5.3 Marine

- 14.5.4 Telecommunication

- 14.6 Asia Pacific GNSS Device Market Value and Volume, by End Use (2021-2033)

- 14.6.1 Commercial Use

- 14.6.2 Personal Use

- 14.6.3 Industrial Use

Chapter 15 Latin America GNSS Device Market

- 15.1 Overview

- 15.2 Latin America GNSS Device Market Value and Volume, by Country (2021-2033)

- 15.2.1 Brazil

- 15.2.2 Argentina

- 15.2.3 Rest of Latin America

- 15.3 Latin America GNSS Device Market Value and Volume, by Technology (2021-2033)

- 15.3.1 Satellite Navigation

- 15.3.2 Differential GNSS

- 15.3.3 Real-Time Kinematic

- 15.4 Latin America GNSS Device Market Value and Volume, by Device Type (2021-2033)

- 15.4.1 Handheld GNSS Receivers

- 15.4.2 OEM GNSS Modules

- 15.4.3 Smartphone GNSS

- 15.5 Latin America GNSS Device Market Value and Volume, by Application (2021-2033)

- 15.5.1 Automotive

- 15.5.2 Aerospace

- 15.5.3 Marine

- 15.5.4 Telecommunication

- 15.6 Latin America GNSS Device Market Value and Volume, by End Use (2021-2033)

- 15.6.1 Commercial Use

- 15.6.2 Personal Use

- 15.6.3 Industrial Use

Chapter 16 Middle East & Africa GNSS Device Market

- 16.1 Overview

- 16.2 Middle East & Africa GNSS Device Market Value and Volume, by Country (2021-2033)

- 16.2.1 Saudi Arabia

- 16.2.2 UAE

- 16.2.3 South Africa

- 16.2.4 Rest of Middle East & Africa

- 16.3 Middle East & Africa GNSS Device Market Value and Volume, by Technology (2021-2033)

- 16.3.1 Satellite Navigation

- 16.3.2 Differential GNSS

- 16.3.3 Real-Time Kinematic

- 16.4 Middle East & Africa GNSS Device Market Value and Volume, by Device Type (2021-2033)

- 16.4.1 Handheld GNSS Receivers

- 16.4.2 OEM GNSS Modules

- 16.4.3 Smartphone GNSS

- 16.5 Middle East & Africa GNSS Device Market Value and Volume, by Application (2021-2033)

- 16.5.1 Automotive

- 16.5.2 Aerospace

- 16.5.3 Marine

- 16.5.4 Telecommunication

- 16.6 Middle East & Africa GNSS Device Market Value and Volume, by End Use (2021-2033)

- 16.6.1 Commercial Use

- 16.6.2 Personal Use

- 16.6.3 Industrial Use

Chapter 17 Company Profiles and Market Share Analysis: (Business Overview, Market Share Analysis, Products/Services Offered, Recent Developments)

- 17.1 Hexagon

- 17.2 Rockwell Collins

- 17.3 Trimble

- 17.4 Garmin

- 17.5 Qualcomm

- 17.6 Magellan

- 17.7 Nokia

- 17.8 Navcom Technology

- 17.9 Skyhook

- 17.10 Huawei

- 17.11 Sony

- 17.12 Stonex

- 17.13 TomTom

- 17.14 ublox

- 17.15 Broadcom

- 17.16 Others

Related Reports

Report ID:

21

Published Date:

March 2025

Trusted by more than 10,500 organizations globally

Infaluble Methodology

Customization

Analyst Support

Targeted Market View