Global Direct-to-consumer Disease Risk and Health DNA Test Market - Size and Forecast Analysis, 2021-2035

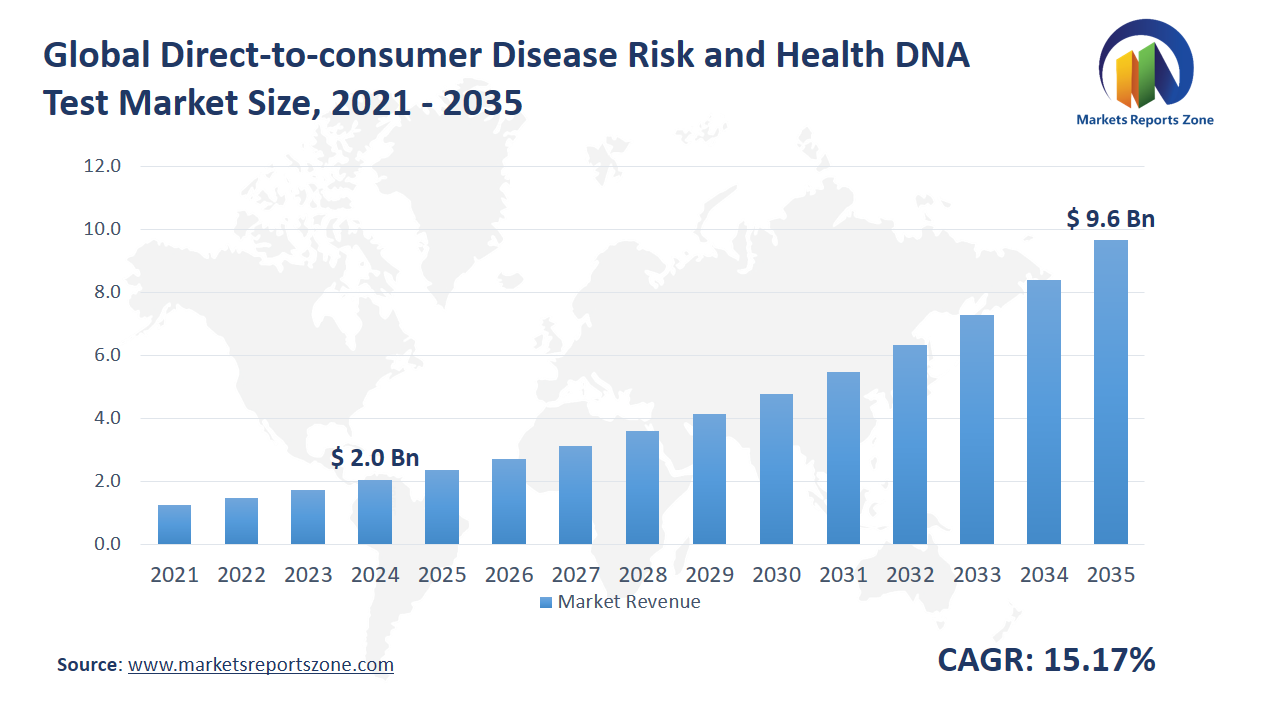

Global Direct-to-consumer Disease Risk and Health DNA Test Market Size is expected to reach USD 9.66 Billion by 2035 from USD 2.04 Billion in 2024, with a CAGR of around 15.17% between 2024 and 2035. The global direct-to-consumer disease risk and health DNA test market has been driven by rising health awareness and growing interest in personalized healthcare. Increased demand for at-home testing kits has been observed due to their convenience and privacy. Consumers have shown greater interest in understanding genetic predispositions to conditions like diabetes and heart disease. However, the market has been restrained by concerns over data privacy and misuse of sensitive genetic information. Regulatory bodies in many countries have raised questions about data handling and consent. Despite this, key opportunities have emerged. Integration of DNA testing with digital health platforms has been encouraged, offering users detailed insights and lifestyle recommendations. Partnerships between DNA testing firms and wellness brands have been formed to expand service offerings. For example, in Japan, elderly consumers have adopted DNA health tests to manage age-related risks through diet plans. In the U.S., fitness-focused consumers have used these tests to optimize training and nutrition based on genetic profiles. Subscription-based health plans tied to DNA results have also gained traction. As awareness spreads and technology advances, direct-to-consumer DNA testing is being viewed as a proactive health management tool, reshaping how individuals engage with their long-term well-being.

Driver: Health Awareness Sparks DNA Test Demand

One of the strongest drivers of the direct-to-consumer DNA testing market is the rising awareness of health and disease prevention. People today are more proactive about understanding their bodies and genetic makeup. This shift has been fueled by a global focus on wellness, early diagnosis, and lifestyle-driven healthcare. Consumers want to know their risk levels for common conditions such as cancer, Alzheimer’s, and autoimmune disorders. This curiosity is not just medical—it’s personal. In South Korea, tech-savvy millennials have turned to DNA kits to tailor their skincare and diet routines based on inherited traits. In Canada, busy professionals have used these tests to manage stress-related health risks through personalized fitness and nutrition plans. At-home testing kits have been chosen for their simplicity and privacy, making health tracking accessible without hospital visits. In urban African cities, young adults have adopted DNA-based health plans to better understand hereditary risks that often go unnoticed. With increased sharing on social media, users have also inspired others to explore their genetic backgrounds. As the link between lifestyle and genetic predisposition becomes more widely understood, DNA tests are no longer viewed as just diagnostics—they’re being embraced as everyday wellness tools.

Key Insights:

- Over 35% of adults in the U.S. have taken at least one direct-to-consumer DNA test.

- A leading genetics company invested USD 400 million in expanding its personal health DNA testing services.

- More than 50 million at-home DNA kits have been sold globally in the past five years.

- In Europe, DNA health tests have achieved a 28% penetration rate among digital health users.

- One major biotech firm allocated USD 150 million to develop AI-based platforms for DNA result interpretation.

- In Japan, over 40% of users aged 60+ have adopted DNA testing for age-related disease risk management.

- A South American government launched a USD 60 million public initiative to integrate genetic testing into primary care.

- Over 65% of direct-to-consumer DNA test users have subscribed to follow-up wellness or nutrition services.

Segment Analysis:

The direct-to-consumer disease risk and health DNA test market is segmented by type and application, reflecting the diversity in consumer needs and conditions targeted. Type I includes general health and risk assessment tests, often used for preventive care and lifestyle planning. Tests specific to Celiac disease have gained popularity among individuals with unexplained digestive issues, especially in countries like Germany, where dietary adjustments are now being made based on genetic feedback. Parkinson’s disease testing has seen demand among individuals with a family history of neurological disorders, particularly in the UK and Scandinavian nations. Alzheimer’s disease risk testing is being used by middle-aged adults in the U.S. and Australia to prepare for long-term health decisions, including diet, mental exercises, and insurance planning. By application, the online segment has become dominant, offering ease of ordering, home delivery, and digital result access. In India, tech-savvy urban users have favored online platforms for DNA test purchases tied to mobile health apps. Meanwhile, the offline segment continues to serve older populations and less digitally engaged users, especially in rural areas of Eastern Europe and parts of Southeast Asia. Together, these segments reflect a market that is not only expanding but also becoming more tailored to individual needs and access preferences.

Regional Analysis:

The direct-to-consumer disease risk and health DNA test market varies significantly across regions, influenced by cultural attitudes, healthcare systems, and digital infrastructure. In North America, particularly the U.S. and Canada, the market is growing rapidly, driven by high health awareness and access to advanced testing services. Consumers use DNA tests for preventive health and lifestyle adjustments, with major cities like New York and Toronto seeing widespread adoption. Europe has seen steady growth, with countries like the UK and Germany leading the way, as health-conscious individuals seek early detection tools for genetic conditions like Parkinson’s and Alzheimer’s. In Asia-Pacific, the adoption of DNA testing is on the rise, especially in countries like China and Japan, where people are increasingly integrating genetics into health management and wellness routines. In Latin America, while adoption is slower, Brazil and Mexico have seen an increase in online DNA testing platforms, with consumers eager to understand genetic predispositions to chronic diseases. The Middle East has witnessed a more cautious but steady interest, particularly in the UAE and Saudi Arabia, where high-income populations are embracing personalized health services. Each region reflects a unique blend of healthcare priorities and technological adoption, contributing to the growing global market for direct-to-consumer DNA testing.

Competitive Scenario:

The direct-to-consumer disease risk and health DNA testing market has seen significant innovation and competition from companies like 23andMe, MyHeritage, and Ancestry.com, each expanding their services to cover a wide range of health conditions beyond ancestry tracking. For instance, 23andMe has enhanced its offerings to include genetic insights on conditions such as Parkinson’s disease and Alzheimer’s, capitalizing on the growing interest in preventive healthcare. MyHeritage and Ancestry.com, traditionally focused on genealogical services, have also ventured into health testing, providing users with personalized reports on genetic predispositions. LabCorp and Quest Diagnostics, established players in the medical testing field, have integrated genetic health testing into their broader healthcare services, allowing patients to access DNA testing through their existing medical provider network. Meanwhile, companies like Invitae and Color Genomics have focused on delivering more medically detailed results, targeting patients and healthcare providers with clinical-grade tests for inherited conditions. Smaller firms like Mapmygenome and Pathway Genomics are carving out niches by offering personalized wellness and health insights. As technology advances, platforms like Gene By Gene and DNA Diagnostics Center are increasingly integrating AI and machine learning to enhance test accuracy. Together, these companies are shaping the future of personalized medicine, driving both innovation and accessibility in DNA-based health solutions.

Direct-to-consumer Disease Risk and Health DNA Test Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 2.04 Billion |

| Revenue Forecast in 2035 | USD 9.66 Billion |

| Growth Rate | CAGR of 15.17% from 2025 to 2035 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2035 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | 23andMe; MyHeritage; LabCorp; Myriad Genetics; Ancestry.com; Quest Diagnostics; Gene By Gene; DNA Diagnostics Center; Invitae; IntelliGenetics; Ambry Genetics; Living DNA; EasyDNA; Pathway Genomics; Centrillion Technology; Xcode; Color Genomics; Anglia DNA Services; African Ancestry; Canadian DNA Services; DNA Family Check; Alpha Biolaboratories; Test Me DNA; 23 Mofang; Genetic Health; DNA Services of America; Shuwen Health Sciences; Mapmygenome; Full Genomes |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Direct-to-consumer Disease Risk and Health DNA Test Market report is segmented as follows:

By Type,

- Type I

- Celiac Disease

- Parkinson Disease

- Alzheimer Disease

By Application,

- Online

- Offline

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East and Africa

Key Market Players,

- 23andMe

- MyHeritage

- LabCorp

- Myriad Genetics

- Ancestry.com

- Quest Diagnostics

- Gene By Gene

- DNA Diagnostics Center

- Invitae

- IntelliGenetics

- Ambry Genetics

- Living DNA

- EasyDNA

- Pathway Genomics

- Centrillion Technology

- Xcode

- Color Genomics

- Anglia DNA Services

- African Ancestry

- Canadian DNA Services

- DNA Family Check

- Alpha Biolaboratories

- Test Me DNA

- 23 Mofang

- Genetic Health

- DNA Services of America

- Shuwen Health Sciences

- Mapmygenome

- Full Genomes

Frequently Asked Questions

How big is the Direct-to-consumer Disease Risk and Health DNA Test market?

Global Direct-to-consumer Disease Risk and Health DNA Test Market Size was valued at USD 2.04 Billion in 2024 and is projected to reach at USD 9.66 Billion in 2035.

What is the Direct-to-consumer Disease Risk and Health DNA Test market growth?

Global Direct-to-consumer Disease Risk and Health DNA Test Market is expected to grow at a CAGR of around 15.17% during the forecasted year.

Which region has the largest market share in Direct-to-consumer Disease Risk and Health DNA Test market?

North America, Asia Pacific and Europe are major regions in the global Direct-to-consumer Disease Risk and Health DNA Test Market.

Who are the key players in Direct-to-consumer Disease Risk and Health DNA Test market?

Key players analyzed in the global Direct-to-consumer Disease Risk and Health DNA Test Market are 23andMe; MyHeritage; LabCorp; Myriad Genetics; Ancestry.com; Quest Diagnostics; Gene By Gene; DNA Diagnostics Center; Invitae; IntelliGenetics; Ambry Genetics; Living DNA; EasyDNA; Pathway Genomics; Centrillion Technology; Xcode; Color Genomics; Anglia DNA Services; African Ancestry; Canadian DNA Services; DNA Family Check; Alpha Biolaboratories; Test Me DNA; 23 Mofang; Genetic Health; DNA Services of America; Shuwen Health Sciences; Mapmygenome; Full Genomes and so on.