Global Battery and Fuel Cell Material Market - Size and Forecast Analysis, 2021-2035

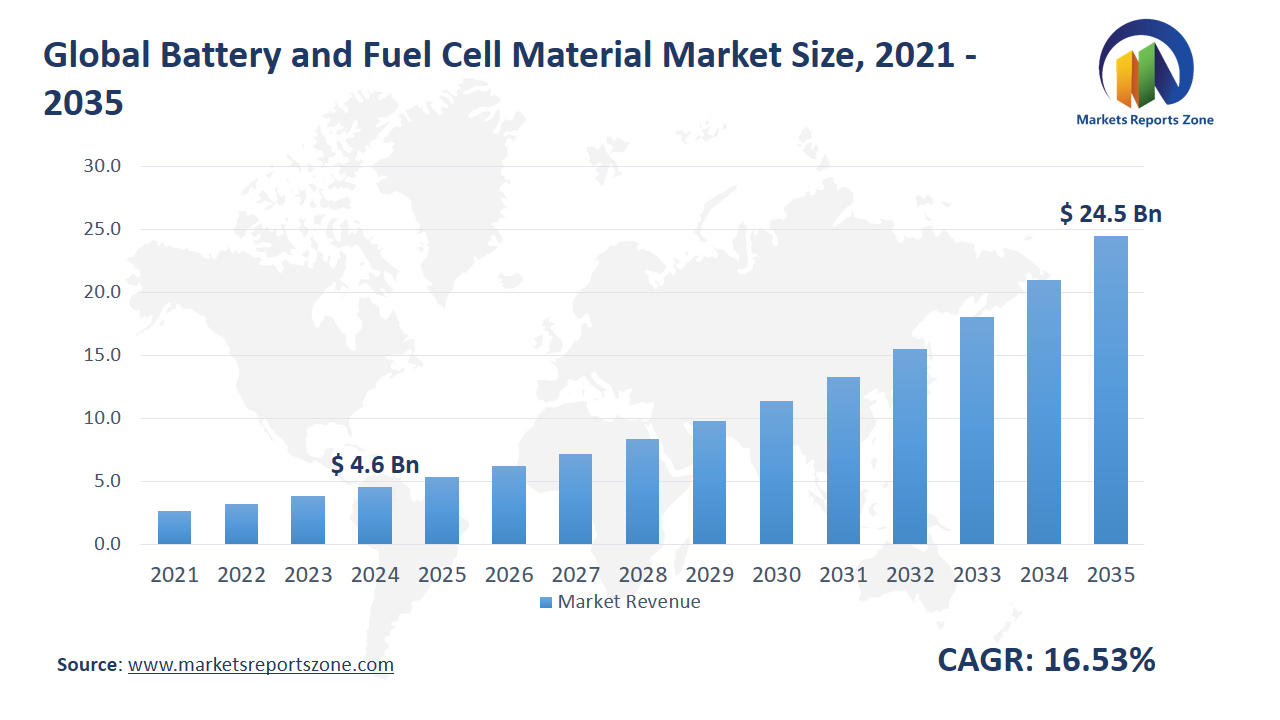

Global Battery and Fuel Cell Material Market Size is expected to reach USD 24.51 Billion by 2035 from USD 4.55 Billion in 2024, with a CAGR of around 16.53% between 2024 and 2035. The global battery and fuel cell material market is being propelled by two key drivers. Firstly, the surge in electric vehicle (EV) adoption has intensified the demand for lithium, cobalt, and nickel. For instance, in India, the expansion of EV manufacturing hubs has led to increased imports of these critical materials. Secondly, the global shift towards renewable energy sources necessitates efficient energy storage solutions, thereby boosting the need for advanced battery materials. In Germany, the integration of wind and solar power into the grid has been supported by large-scale battery storage systems. However, the market faces a significant restraint due to the high costs and environmental concerns associated with mining these essential materials. In the Democratic Republic of Congo, cobalt mining has raised ethical and ecological issues, impacting supply chains. Despite these challenges, opportunities abound. One such opportunity lies in the development of alternative battery technologies, such as sodium-ion batteries, which are being explored in China to reduce reliance on scarce resources. Another opportunity is the advancement of recycling technologies. In Japan, companies are investing in battery recycling facilities to recover valuable materials, promoting a circular economy. These developments indicate a dynamic market adapting to both challenges and opportunities.

Driver: Electric Vehicles Drive Material Demand

The rising adoption of electric vehicles has strongly driven the demand for battery and fuel cell materials across the globe. With more countries pushing for reduced carbon emissions and cleaner transportation, EV production has surged in both developed and developing nations. This shift has created high demand for lithium, cobalt, nickel, and graphite—key materials used in lithium-ion batteries. In the United Kingdom, major automakers have announced the transition of their vehicle lines to fully electric by the end of the decade, leading to significant investment in battery material sourcing. In South Korea, new battery plants have been constructed to meet the demands of local and export EV markets, resulting in increased imports of refined nickel and lithium. Meanwhile, in Australia, mining operations have been expanded to meet global lithium supply gaps. This trend has created ripple effects through supply chains, increasing research in extraction efficiency and battery performance. Automakers are forming direct partnerships with material suppliers to secure stable sources, showing how deeply this driver is shaping the market. As EV sales continue to rise, the push for high-performing, sustainable battery materials will remain a critical force behind the battery and fuel cell material industry’s growth.

Key Insights:

- Over 120,000 tons of lithium-ion battery materials were consumed globally for electric vehicles in 2024.

- The adoption rate of advanced battery materials in the automotive industry exceeded 60% in Asia-Pacific by 2024.

- Government investment in battery and fuel cell material research in the U.S. surpassed $400 million in 2023.

- Over 1,500 tons of fuel cell materials were supplied to stationary power projects worldwide in 2024.

- The penetration rate of fuel cell materials in stationary power generation reached 18% among new installations in Japan in 2024.

- Bloom Energy shipped more than 600 MW of solid oxide fuel cell systems, using over 2,000 tons of specialized materials in 2024.

- China produced over 80,000 tons of battery-grade graphite for EVs and energy storage in 2024.

- The adoption rate of battery materials in consumer electronics manufacturing reached 72% in North America in 2024.

Segment Analysis:

The battery and fuel cell material market is segmented by type and application, with each category playing a vital role in performance and innovation. Among material types, metals are being widely used in current collectors and electrodes due to their high conductivity. In Sweden, a local battery manufacturer has shifted to using aluminum and copper sheets for lightweight and efficient current collection. Polymers are being utilized in separators and flexible containers, offering improved thermal resistance. A factory in South Korea has started using advanced polymer films in pouch-cell batteries to ensure better safety in consumer electronics. Carbon and graphite remain essential, especially in anodes, where high conductivity and stability are critical. In Turkey, graphite is being sourced and refined domestically to reduce import dependency for lithium-ion cell manufacturing. In terms of application, active materials like cathodes and anodes are receiving significant focus for improving energy density. In Vietnam, research labs are developing new lithium iron phosphate compounds for longer-lasting batteries. Electrolytes are also evolving, with solid-state alternatives being tested in Canada to reduce flammability risks. Containers, often overlooked, are being redesigned with lightweight composites to enhance battery efficiency in drones and small EVs. Each segment contributes uniquely, reflecting global efforts toward better, safer energy storage systems.

Regional Analysis:

The battery and fuel cell material market is evolving differently across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In North America, strong investments in EV production and government-backed energy storage projects have accelerated demand. In the U.S., new battery plants are being built in states like Georgia to support electric truck manufacturing. In Europe, strict emission regulations and a strong focus on sustainability have driven innovation in material sourcing. In France, recycled battery materials are being integrated into mainstream supply chains to reduce environmental impact. Asia-Pacific remains the manufacturing hub, with China, Japan, and India scaling up production. In Indonesia, domestic nickel mining has been expanded to supply regional battery factories. Latin America is emerging as a key source of raw materials. In Chile, lithium is being extracted with new eco-friendly techniques to support global supply. Meanwhile, in the Middle East & Africa, gradual industrialization and renewable energy initiatives are opening new markets. In Morocco, green hydrogen projects are being connected with fuel cell development, encouraging local use of advanced materials. Each region contributes uniquely—either through production, innovation, or raw material supply—making the global market both interconnected and heavily dependent on regional strengths and resources.

Competitive Scenario:

The global battery and fuel cell material market is being shaped by key players implementing innovative strategies and facing industry challenges. Exide Technologies has introduced the Solition Material Handling battery, utilizing lithium iron phosphate technology to enhance reliability and energy efficiency in industrial applications like forklifts and automated guided vehicles. Cabot Corporation is expanding its footprint by investing approximately $200 million to increase U.S. production capacity for conductive carbon additives, essential for lithium-ion batteries, and has launched the LITX® 93 series to improve battery conductivity and performance. BASF is focusing on sustainability by starting a prototype metal refinery in Schwarzheide, Germany, to recover valuable metals from end-of-life lithium-ion batteries, aiming to support a circular economy in battery materials. Additionally, BASF has partnered with SK On to explore collaboration opportunities in cathode active materials, targeting the North American and Asia-Pacific markets. While specific recent developments for Eco-Bat Technologies, Doe Run Company, and Hammond Group are not detailed in the provided information, these companies continue to play roles in the battery materials supply chain. Overall, the industry is witnessing significant investments and collaborations aimed at enhancing battery performance, sustainability, and supply chain resilience.

Battery and Fuel Cell Material Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 4.55 Billion |

| Revenue Forecast in 2035 | USD 24.51 Billion |

| Growth Rate | CAGR of 16.53% from 2025 to 2035 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2035 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | Exide Technologies; Eco-Bat Technologies; Doe Run Company; BASF; Cabot Corporation; Hammond Group |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Battery and Fuel Cell Material Market report is segmented as follows:

By Type,

- Metals

- Polymers

- Carbon/Graphite

By Application,

- Active Materials

- Current Collectors

- Containers

- Electrolytes

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East and Africa

Key Market Players,

- Exide Technologies

- Eco-Bat Technologies

- Doe Run Company

- BASF

- Cabot Corporation

- Hammond Group

Frequently Asked Questions

How big is the Battery and Fuel Cell Material market?

Global Battery and Fuel Cell Material Market Size was valued at USD 4.55 Billion in 2024 and is projected to reach at USD 24.51 Billion in 2035.

What is the Battery and Fuel Cell Material market growth?

Global Battery and Fuel Cell Material Market is expected to grow at a CAGR of around 16.53% during the forecasted year.

Which region has the largest market share in Battery and Fuel Cell Material market?

North America, Asia Pacific and Europe are major regions in the global Battery and Fuel Cell Material Market.

Who are the key players in Battery and Fuel Cell Material market?

Key players analyzed in the global Battery and Fuel Cell Material Market are Exide Technologies; Eco-Bat Technologies; Doe Run Company; BASF; Cabot Corporation; Hammond Group and so on.